2027 Proposed Individual Health Insurance Rates

The Office of the Insurance Commissioner has released the proposed individual rates for 2027. A consumer can even comment about the proposals on the OIC’s Webpage. It’s a very good idea to give feedback. Last year we saw a massive jump in rates and we are seeing a repeat with the lack of positive legislation.

If you want to make a comment then head to the OIC’s page and you can make comments on each company.

The factors are pretty important.

- The loss of the Enhanced Tax credits has drove the uninsured number higher which costs to providers who pass on the cost to the consumer. These impact rural families, small businesses and early retirees the most. It directly impacts millions of Americans.

- The Medical Loss Ratio. A individual insurance company must spend at least 80% of premiums on healthcare or they rebate the owner of the policy. There isn’t a single insurance company that was under 80%. For a successful change to occur then Provider and Pharmaceutical prices have got to be addressed.

- The massive loss of enrollments. A record number have disenrolled compared to last year.

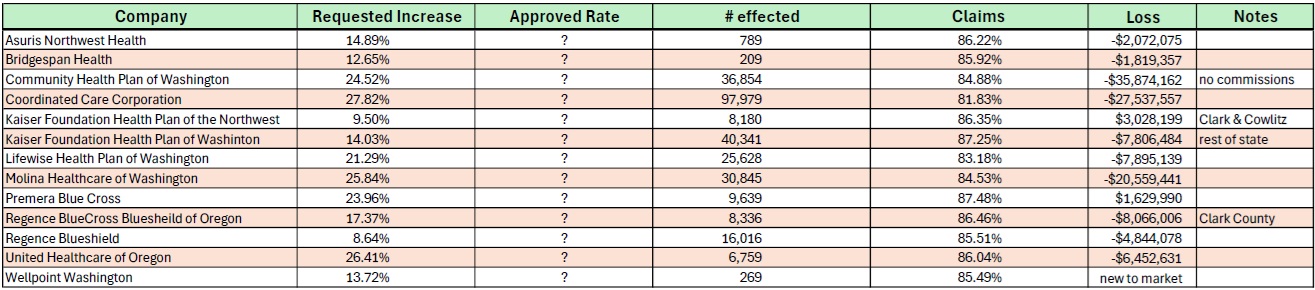

These are not the final rates. The average requested rate is 22.4% and individual plans could shift very differently that the overall picture. They have to be approved by the Office of Insurance then approved by the Healthplanfinder.

There are plans that are choosing to de-commission so consumers will have fewer options for customer service. The more plans that offer fewer commissions, it makes it a challenge to keep lights on for community resources. Some agents may drop out or start charging fees. We do our best to offer additional types of insurance to fill in the gaps and allow our health agents to continue despite an Insurance company failing to compensate.

Select your appointment early.

Medicare Annual Enrollment is October 15th through December 7th

Healthcare Open Enrollment is November 1sth through December 15th.