Imagine you are on a road trip and your motorcycle suddenly breaks down. You may find yourself stranded with no easy way to get home or reach a repair shop. In some cases, your motorcycle insurance policy may help cover certain expenses, depending on the type of coverage you carry.

At Wenatchee Insurance Agency, we work closely with our clients to ensure they have coverage that fits their riding habits and travel plans. If you need motorcycle insurance in Wenatchee, WA, our team is ready to help you explore your options and request a quote.

When Motorcycle Insurance Can Help During a Breakdown

Standard motorcycle insurance policies usually provide limited assistance when a bike breaks down due to mechanical issues. However, if you have roadside assistance coverage, you may be able to request help. This optional add-on can provide services such as towing your motorcycle to a nearby repair shop, jump-starting a dead battery, changing a flat tire, or delivering fuel if you run out.

Another valuable option is trip interruption coverage. This add-on may reimburse certain expenses related to a covered breakdown, such as lodging, meals, or transportation costs, if your trip is cut short. Towing and labor coverage can also help pay for the cost of transporting your motorcycle to a repair facility so it can be serviced as quickly as possible.

Get the Motorcycle Coverage That Fits Your Needs

When reviewing your motorcycle insurance options, it is important to understand which coverages are included and which may need to be added. The team at Wenatchee Insurance Agency is here to help. For motorcycle insurance in Wenatchee, WA, contact us today to review your policy and make sure you have the protection you need before your next ride.

Wenatchee Insurance is an independent insurance agency located on Mission Street in Wenatchee Washington . We write policies with a variety of companies for our customer’s needs. Yes, we can insure your apartment, care, and health along with your motorcycle.

If you’re a property owner in Washington State, you know that it’s wise to protect your investment in that property by purchasing property insurance. If your property is in Central Washington, our team at the Wenatchee Insurance Agency invites you to meet with us and explore our wide range of property insurance options.

Leaks, Water Damage, and Mold

According to the Office of the Washington State Insurance Commissioner, water damage is one of the most frequent reasons for a property insurance claim. The same website reports that when and why your property is damaged will make an impact on whether your water damage or mold infestation is covered by your insurance. Although it’s typically easy for property owners to discover a sudden leak, gradual leaks are often overlooked or undiscovered until significant damage has occurred. If a storm makes a hole in your structure, you’ll want to get it repaired as soon as possible.

According to the Office of the Washington State Insurance Commissioner, although excess water buildup may be responsible for mold infestations, a standard property insurance policy will not typically cover mold damage, rust, or rot. In some cases, your insurance may cover those damages if you can show that it was caused by water damage. Some property insurance policies offer limited mold damage coverage. Talk to one of our insurance agents for more information.

Call Us for Your Appointment Today

Property owners can’t predict the future, but they can prepare for it. Our team at the Wenatchee Insurance Agency understands your need to be prepared for any eventuality. Property owners in or near Wenatchee, WA, have discovered that we provide excellent customer service. Call us about your appointment today, and let’s talk about insurance.

When you purchase insurance for your ATV or snowmobile, you expect it to cover your vehicle. But there are always exceptions and exclusions in insurance policies. Doing your due diligence when seeking out insurance for snowmobiles and ATVs is of the utmost importance. For example, if you have a customized ATV or snowmobile, is it going to be covered by the basic insurance policy you plan on purchasing? Here’s what you need to know about the limits of standard insurance policies for snowmobiles and ATVs, and how the team here at Wenatchee Insurance Agency, serving Wenatchee, WA, can help you get the coverage you need.

Will a Standard Policy Cover Customized Snowmobiles and ATVs?

As is the case with most standard policies designed to cover various types of recreational and traditional vehicles, your standard policy isn’t going to offer the comprehensive coverage needed for customized snowmobiles or ATVs. This is because insurance is traditionally designed to cover the full value of the vehicle itself, not any aftermarket modifications that may bump up the value significantly. That being said, you don’t have to go without coverage or go without customizing your vehicle. Many insurance policy providers for snowmobiles and ATVs will offer policy add-ons so you can get the extra coverage you need for any modifications you make. Just remember to update your insurance company with these changes as they take place to avoid claim denials in the future.

Not all all snowmobiles are the same especially in North Central Washington. We have events like Snowfest in Leavenworth where we can meet other powersport fans. Or heading up the Methow and experiencing the trails around Winthrop. If you are dropping in a new can for a more aggressive sound or fine tuning your suspension to reduce body roll then you want those new parts covered.

Cover Your Snowmobile or ATV With Wenatchee Insurance Agency

Whether your snowmobile or ATV is modified or not, you can rely on us at Wenatchee Insurance Agency, serving Wenatchee, WA, to find the appropriate insurance policy for you. Start now, and compare quotes with us!

The 2026 rates have been approved and are visible for the first time on the Washington Healthplanfinder. As I write this post the Silver plans were not loaded and you can not compare them side by side with your 2025 plans. All of the 2026 plans are listed on the Office of the Insurance Commissioner.

2026 rates first look

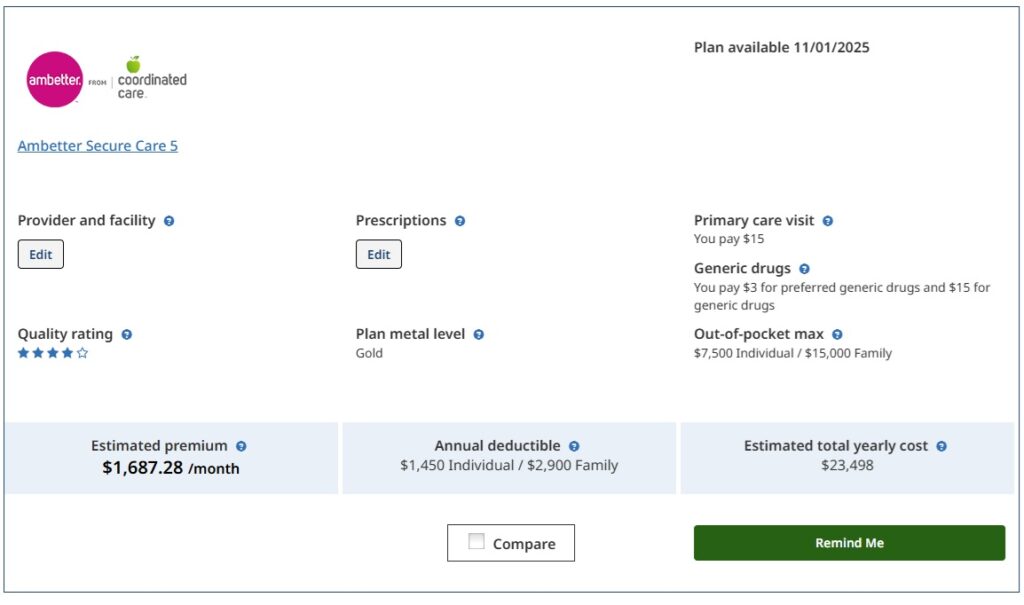

This is off the main screen from the Washington Healthplanfinder. It is only an estimate. It can change depending on what Congress does regarding the enhanced tax credits and the Healthplanfinder. When the enhanced tax credits were introduced, the first month that they went into effect was June of 2021. It made quite a difference in keeping money in the pocket’s of American households.

Our household is no longer eligible for tax credits with the current plan from Congress. So we have to make the jump from a couple hundred dollars to approaching $1687 per month. As small business owners, we don’t have the luxury of a large group plan. It will be about 1/4 of our income for 2026 before we get into use.

The Health Open Enrollment Period is important to talk about. The plans have made some big shifts and if you are eligible for tax credits will be more manageable. It is important to talk with someone who has a greater understanding of insurance than “that Uncle” eight into a case at Thanksgiving.

November 1st through December 15 for health plans starting January 1st

December 16 through January 15th for health plans starting February 1st.

Medicare has it’s own enrollment periods and there are special enrollments. We run applications year round just in case we find a Special Enrollment that works or to prepare for the next open enrollment.

Every year it is important to look at your plan because of changes. There are times that plans do not automatically renew or need to be updated. If a plan leaves the area then you may have been moved over to a plan that doesn’t work as well.

At Wenatchee Insurance Agency, we like to review plans every year during the Open Enrollment Period. This is Matt’s 13th Open Enrollment. We walk through all the plans available. We do not charge broker fees and if any commission is available it comes from the insurance company.

One of the first people that Suzie enrolled was a refugee from Central America. It was an incredibly dangerous journey and they were needing medical attention to recover. Without Apple Health, they would not have received the care that they needed.

During Trump 1.0, Matt had a mom refuse to complete an application for their children over fear of the father being deported. That is a monstrous choice that no mother should have to make that he witnessed first hand. It’s why we are very protective of data and who we hand it over to.

Yes, some very cruel individuals like to threaten folks with public charge with all programs. It is important to note: The public charge rule will not consider any other federal or state benefits. That includes SNAP, WIC, CHIP, school lunches, Medicaid, Section 8 housing benefits, food banks, shelters, COVID-related medical care, and many more. So sometimes even we can not overcome fears on what will be used against families.

We can say that we have a couple of the insurance nerds at the office that used to ran one of the enrollment centers so we are real familiar with the Healthplanfinder for immigrants and the data that goes back and forth there. They don’t exchange medical data. There is a couple of Federal Hubs that they verify data with however those require the SSN.

The information is used for enrollment and states right on the front page it will not be used for immigration enforcement.

Medicaid falls under the Healthcare Authority’s control. If you don’t have access then here is a better description on what was taken.

The following programs were impacted by the breach:

Alien Emergency Medical

Apple Health Expansion

Civil Transitions

Non-Citizen Pregnant Women

Medicaid Family Planning (Take Charge)

The Alien Emergency Medical is a catastrophic program like dying of Cancer level patients. It’s one that no one wants to be on but delivers care to the patient and funds to the providers.

We don’t work directly with Civil Transitions, Non-Citizen Pregnant Women and Medicaid Family Planning as there are some programs that are not common on the Healthplanfinder.

Undocumented Immigrants make up about 24% of the uninsured in Washington State. Which is a priority to gain coverage to reduce the uninsured rate in the state.

At the office level, data is kept encrypted and not sold or shared expect to enroll people into insurance plans. We do everything in our power to prevent data breeches at a local level.

It is going to take the Legislatures at the STATE level to do something to prevent data from being stolen again.

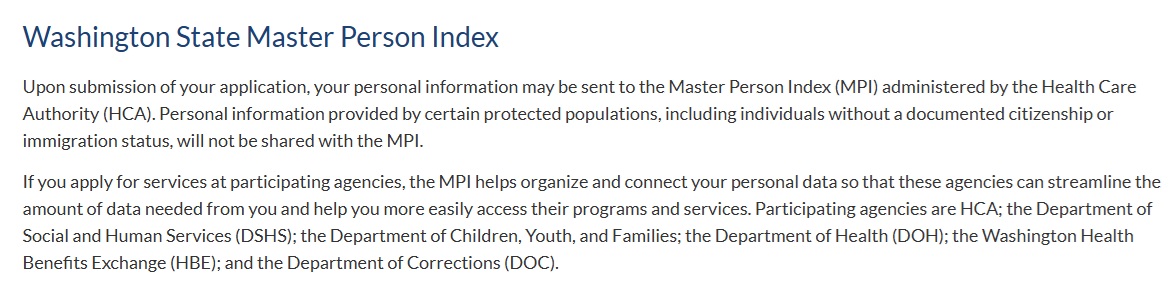

The Washington Healthplanfinder Privacy Notice talks about their commitment to Privacy and provides contact information if you would like further assistance. The Master Person Index (MPI) is administered by the Healthcare Authority. Here is their statement:

Matt has been assisting people with Health Insurance since the first year of the ACA. Suzie and Matt ran the Enrollment Center for years in Wenatchee assisting people enroll in Health Insurance without adding fees. We work with Wenatchee Insurance which is an independent insurance agency.

It is that time of year when the Office of Insurance let’s people know what the health insurance rates could do for the following year. From our experience, we knew that big changes were going to occur for a couple of reasons.

Asuris Northwest Health is requesting a 15.15%. With 964 people enrolled they lost $1.2 million with a claims of 85.81%. This is an off exchange plan that does not get additional help from premium tax credits. Here is where you comment.

Bridgespan Health Company is requesting a 18.38% increase. With 376 people enrolled they lost $1.1 million after the $2.2 million risk adjustment. Here is whereyou comment.

Community Health Plan of Washington is requesting a 27.57%. With 34,463 people enrolled they lost $16.9 million after a $44.2 million risk adjustment. They have eliminated broker commissions. Here is where you comment.

Coordinated Care Corporation is requesting a 21.95% With 107,649 people enrolled they lost $1.3 million after a risk adjustment loss of $68.1 million and a claims of 80.94%. They are maintaining broker commissions for customer service. Here is where you comment.

Kaiser Foundation Healthplan is requesting a 11.36%. With 7,000 people enrolled in Clark and Cowlitz the company made $5.5 million after the risk adjustment and a claims of 85.5%. Here is where you comment.

Kaiser Foundation Health Plan of Washington is requesting a 19.18%. With 40,266 enrolled they lost $360,419 after a $3.1 million loss in risk adjustment however the claims were 88.88%. Here is where you comment.

Lifewise Health Healthplan of Washington is requesting a 14.43%. With 23,727 people enrolled in this non-grandfathered plan, they made $3.5 million after a $13.3 million risk adjustment loss. However their claims were 89.39%. Here is where you comment.

Lifewise Health Plan of Washington is requesting a 10.4%. They have 1843 people enrolled in their grandfathered plan and made $1.0 million with this closed book. Here is where you comment.

Molina Healthcare of Washington is requesting a 24.59%. They have 43,346 enrolled and made $6.6 million after a $40.1 million loss from risk adjustment. Their claims was 83.1%. Here is where you comment.

Premera Blue Cross is requesting a 18.79%. With 9,460 enrolled, they made $8.1 million after a risk adjustment of $41.5 million. They had 92.57% in claims. Here is where you comment.

Providence Health Plan is requesting a 10.59%. With 254 people served, the company made $558,805 after the risk adjustment. Here is where you comment.

Regence Bluecross Blueshield of Oregon is requesting a 24.93%. With 10,029 people served in Clark County they lost $6.5 million after a risk adjustment of $5.3 million. With claims coming in at 86.87%. Here is where you comment.

Regence Blueshield is requesting a 9.6%. With 21,878 enrolled, they lost $14.3 million after a risk adjustment loss of $31.8 million. They also have a claims of 86.41%. Here is where you comment.

United Healthcare of Oregon is requesting a 37.35%. With 6180 enrolled they lost $9.2 million after a $2.6 million loss from risk adjustment. They also had a claims of 86.20%. Here is where you comment.

How to prepare for fall enrollment

Open Enrollment for Health Insurance runs from November 1st through December 15th.

1. I want their training. They get trained by the insurance companies on how the plans function. They have to keep up on their training and have an expertise that you don’t get casually. Your Aunt Betty who worked with insurance ten years ago may not have understand any updates to the industry.

2. They carry insurance on their decision that I don’t have. Professionals that advise people carry insurance. It provides an extra layer if things go wrong.

3. If the insurance company goes sideways then I have someone to assist me in filing a complaint. This is why I use someone contracted with multiple companies. I want my agent to be able to use options.

4. They would be able to tell you particulars about what is going on for a brand in an area. For example, they would know if there is any problems with the local clinic’s contract with Kaiser.

5. They do not fall into the brand trap. You may have had a particular dental plan for years. Folks around you use the same named company with great success. What happens if you grab the cheap version that doesn’t cover what you need?

6. There are differences that you should know.

In Washington State a Producer or agent is what most people will work with. They can be contracted with one or multiple companies.

For Health Insurance, you can work with a navigator who is unlicensed and can not advise you what plans that you can pick. You can also work with a broker, who is licensed, can advise you and fill in any gaps with additional coverage. Both are called in person assisters.

An Insurance Broker is commonly thought as someone who works with multiple companies. Some will have a Surplus Lines Broker to work with more exotic policies. Health Insurance Agents that work with the State Exchange are referred to as brokers. Since brokers don’t represent insurance companies, they can’t bind coverage on behalf of an insurer when purchasing insurance. They must hand over the account to an insurer or insurance agent to complete the transaction.

If you are not able to get a Health Insurance plan now because it is special enrollment then you would be in a better position November 1st when Open Enrollment begins.

An agent (producer) is a vital tool in assisting you shop for an insurance plan. They will have insight into plans from their training and experience. If you can have a conversation with them then you are off to a good start in finding a plan that suits your needs.

Why You Should See Shayla at Wenatchee Insurance for a Surety Bond (And Avoid the DIY Disaster)

Let’s talk about bonds. No, not the kind James Bond carries around in his secret spy wallet—though that would be cool. We’re talking about surety bonds, contractor bonds, notary bonds, and all the other fun financial guarantees that businesses and individuals sometimes need. If that sounds about as exciting as watching paint dry, don’t worry—Shayla at Wenatchee Insurance makes the process painless, simple, and, dare we say, almost enjoyable.

Surety Bonds Are Confusing. Shayla Is Not.

If you’ve ever tried to Google “how to get a surety bond in Washington state,” you probably ended up in a confusing rabbit hole of legal jargon, application forms, and requirements that make no sense. That’s because bonds involve three parties—the principal (you), the obligee (the entity requiring the bond), and the surety (the insurance company backing it). Still with us?

Good news: You don’t need to memorize any of this. Shayla already knows it all. She translates “insurance-speak” into plain English so you understand exactly what you need and why. No more guesswork, no more frustration—just straightforward answers.

Speed Matters—And Shayla Delivers

Need a bond fast? Maybe you just landed a big job as a contractor and need a license bond yesterday. Or perhaps you suddenly realized that your business permit requires a specific bond you didn’t even know existed. Instead of panicking, just call Shayla. She works quickly to get you bonded ASAP so you can move forward with your business (and avoid that scary fine from the state).

Plus, trying to go it alone can lead to mistakes. A small paperwork error could mean delays, rejections, or worse—paying too much for a bond that doesn’t even cover what you need. Shayla knows how to navigate the system, ensuring you get the right bond at the best price, with zero headaches.

Sure, you could go online and try to get a bond through some faceless website. But do you really want to deal with a call center in who-knows-where when something goes wrong? With Shayla, you’re working with someone who understands Wenatchee, North Central Washington, and all the specific requirements of our state.

More importantly, she actually cares. Need a reminder when your bond is about to expire? She’s got you covered. Not sure if your business needs additional bonding? She’ll walk you through it. Try getting that level of service from a random internet company.

The Bottom Line: Call Shayla

If you need a bond, don’t make it harder than it has to be. Skip the stress, save time, and go straight to the expert. Call or visit Shayla at Wenatchee Insurance—because when it comes to bonds, it’s always better to have a local expert in your corner.

Need help today? Shayla’s ready—give her a call before you find yourself tangled in a web of bond confusion!

Why Working with a Health Insurance Broker Like Suzie or Matt Just Makes Sense (and Cents!)

Because insurance jargon can be confusing, we are talking about insurance producers who work with several different companies.

Navigating health insurance is like walking through a maze of paperwork, confusing terms, and deadlines that feel impossible to hit without a little help. Enter Suzie or Matt from Wenatchee Insurance! Having an insurance broker on your side is like having a GPS that not only gets you where you need to go but also tells you where the free snacks are along the way. Here’s why teaming up with a broker can be the best decision you make for your health—and your sanity.

Reason #1: Brokers Do the Homework for You (So You Can Actually Relax!)

Imagine you’re sitting at your kitchen table, staring at a pile of health insurance pamphlets, each one promising to be just what you need. But which one actually is? That’s where Suzie (or Matt, he’s a gem too) shines! Brokers are like insurance detectives, decoding complex policies to find the plan that’s best for you.

Suzie once helped a client who thought “deductible” was just another word for “tax return,” and “copay” was some sort of buddy system. It turns out, the client didn’t just need insurance; they needed a translator. Suzie swooped in, found a plan that met all their needs, and explained everything in plain English. No more guessing games, no more jargon—just clear, simple guidance.

Reason #2: Brokers Have a Personal Stake in Getting You the Best Deal

Insurance brokers aren’t tied to any single company, so they genuinely care about getting you the best bang for your buck. Suzie and Matt love nothing more than saying, “Yes, that plan is great—and yes, it actually covers that!”

Matt’s favorite story? He once found a plan for a client that covered everything from acupuncture to chiropractic care. The client was thrilled! He had been on the hunt for months, but every plan he came across either had sky-high premiums or the coverage wasn’t quite right. Matt did some digging, called around, and managed to find a plan that was basically a one-stop shop for the guy’s wellness needs. That’s the power of a broker: they go beyond the generic recommendations to find you that perfect match.

Reason #3: Brokers Are Not Robots—They Actually Listen!

Unlike a certain popular insurance website with an “instant quote generator,” Suzie and Matt will actually listen to your needs. Brokers make it their mission to know what’s important to you, like making sure that your favorite doctors are in-network or ensuring your child’s allergies are covered without a hassle.

Imagine Suzie, notebook in hand, jotting down your concerns like an insurance detective. She’s not just a broker; she’s like your insurance BFF. If you’re worried about unexpected medical bills, Suzie will find ways to minimize those costs. If you’re in a health club or have a wellness routine, she’ll find a plan that rewards you for staying healthy.

Reason #4: Peace of Mind, Especially When Life Happens

When your health is on the line, having someone knowledgeable to turn to is invaluable. And Suzie and Matt aren’t just there for the enrollment process. They’re your go-to for questions, claims, and even random inquiries like, “Will this cover my acupuncture for my dog?”

In a world of confusing options, Suzie and Matt at Wenatchee Insurance stand out by offering personalized help, a bit of humor, and plenty of wisdom. So why go it alone? Let Suzie or Matt be your guide—you’ll be in safe hands, with maybe a laugh or two along the way!

Nancy, a resident of the bustling town of Wenatchee, sat staring at an open laptop flashing an array of confusing premium options for her potential health care coverage for the upcoming year. Not only was the screen dizzying to her, but the monthly premiums felt like a gut punch given her household budget. While staring blankly at the screen, the pressing question of how can you get health insurance she can afford weighs heavily on her mind. This is a common thread of worry among many of our Chelan County neighbors during this open enrollment season, especially when you think about what your kids need. As she began looking at the screen, searching for clarity, she wondered if there were any free plans that her neighbor had talked about. Nancy represents the legion of Washingtonians battling the confusion over health care costs. Especially when insurance companies get involved. But like most, she was unsure what to do and definitely didn’t want to put her contact information into a website knowing what would happen to her phone in the aftermath. If only she could find a solution to her health plan options.

What is Free Health Insurance?

With the arrival of open enrollment (November 1st) , Washingtonians are faced with pivotal decisions regarding their health insurance for the coming year. The Suzie @ Wenatchee Insurance and our other agents are inundated with concerns about soaring prices and questions about whether a doctor is covered by individual health plans. The relentless queries, dominated by the pressing question, “Can you get free health insurance in Washington?” echo through our office. This concern is not unfounded. Many residents wonder if the concept of free health care is a tangible reality or a mere mirage in the desert of healthcare options. During this period, the uninsured ponder whether they are flirting with financial peril, and the question of “Is it a scam?” is a regular chorus.

Who Can Get Free Health Insurance in Washington State?

It turns out that free health insurance in Washington isn’t a mythical creature—it does exist for those who fit the mold. Washingtonians may qualify for various health insurance programs at no cost, from government-sponsored initiatives to specific plans within the ACA Marketplace. This means that free health insurance isn’t just a fleeting hope but a tangible reality for some, provided they meet the necessary eligibility criteria, which include specific income requirements and participation in government programs. And even if free isn’t available, an affordable health plan may be within reach.

Washington Residents: Discover If You Can Really Get Health Insurance at No Cost!

Do I Have To Have Health Insurance In Washington?

While Washington State doesn’t impose a penalty for those sans health care coverage, many like Nancy understand that this freedom comes with its own risks. The absence of a safety net can lead to financial turmoil in the face of unexpected medical issues. It’s not mandated, but the sheer unpredictability of life steers many towards exploring the various alternative health plan options available, such as private health plans or policies from ACA Exchange, to mitigate the potential financial strain. But we still have many adults without health insurance in this state.

Types of Health Insurance Available in Washington

Washingtonians are presented with many healthcare program options. From the Marketplace Exchange brimming with plans to the security offered by off-exchange plans, there’s something for everyone. Wenatchee Insurance recommends maintaining some level of health care coverage because, as life has proven time and again, it can indeed come at you fast.

ACA Marketplace Exchange Plans

For many residents, ACA Marketplace or Exchange Plans are a place of hope for containing the cost of health insurance. The costs of marketplace coverage can be offset by federal government subsidies, which is a massive benefit for families struggling with the pressure of inflation. An added benefit is that eligibility for these plans cannot be denied for any pre-existing conditions or for people with disabilities. The Washington Healthplanfinder is an integral part of the healthcare landscape in Washington, ensuring a safety net is available for those who need it most.

Short Term Medical Plans

Short Term Medical Plans are not offered in Washington state. The Washington Office of Insurance would love for you to notify you if someone is offering a short-term plan.

Catastrophic Health Plans

As of July 2024 there were no Insurance Companies offering a Catastrophic Healthcare Plan in Washington State. When they have been available they had an age limit of under 30. Strangely, the majority of people asking for them were over that age.

Requirements for Free Health Insurance in Washington

Free health care services in Washington isn’t a giveaway—it’s a carefully regulated benefit with specific qualifying criteria based on age and income. Programs like Apple Health (Medicaid) or CHIP have stringent eligibility requirements, and while the ACA Marketplace is more broadly accessible, the cost of plans is influenced by a range of qualifying factors. And just because your monthly premiums are free, you can still have costs for doctor visits or hospital care. Let’s look at the three major requirements.

Income Requirements

The pathway to free health insurance in Washington is paved with household income requirements. It’s essential to understand the various types of income, from unemployment benefits to monthly income, which are taken into account when determining eligibility for programs like CHIP and other free health insurance options. If your family is at or below the federal poverty line from an annual income estimate, you will be in line to qualify for Apple Health or CHIP. If your annual household income is above that amount, your household may qualify for Cascade Savings which are state credits that can further reduce your premium cost in some cases to zero.

Age Requirements

Age is a determining factor for free health insurance eligibility in Washington State. For children and young adults, Apple Health and CHIP offer low-cost solutions, while seniors find assistance through Medicare. The Health Insurance Marketplace also provides age-specific options, ensuring a broad spectrum of coverage possibilities for Washingtonians.

Resident Status

The final piece is your status as a permanent resident of Washington. If you have a home in another state where you file your taxes, your ability to obtain a Marketplace or Exchange plan here in Washington is removed no matter how limited your household income might be. It’s vitally important to understand this if you are seeking financial assistance with your health care plan.

We understand that all of this can be incredibly confusing. Nancy certainly was confused by not only choosing a primary care doctor, but also the types of plans available. Local, experienced health insurance agents are the allies Washington need when navigating the complex world of health insurance. They not only understand the individual insurance options available to you, but they also understand which health care providers accept which affordable health insurance plan. And sometimes, a low-cost plan may serve better than a no-cost option. If your objective is to minimize total out-of-pocket expenses, not just monthly premiums, these affordable health service options must be considered. Wenatchee Insurance employs experts who can help tailor the right plan for your individual needs.

Speak to Wenatchee Insurance

At Wenatchee Insurance, our independent agents work tirelessly for the people of Washington. We strive to provide the education necessary to navigate the myriad of options available. Our goal is to pair you with a plan that not only covers your healthcare needs but also aligns with your financial situation.

For Nancy and countless others, the journey to uncover the right health insurance is laden with questions and uncertainties. Click the Button Below to Navigate Through Washingtons’ Health Insurance Plans and Find Out If Free Coverage Is in Your Future! Let us help you demystify the options and uncover the path to your ideal health insurance plan for 2024 and beyond.

Topics: health insurance, ACA, catastrophic health coverage, ACA Alternatives, prescription coverage, private health insurance, short term, apple health, DACA, Okanogan, Grant, Chelan, Douglas, Quincy,

For nearly a decade we have assisted with Health & Medicare Solutions. We are proud to be selected by the Washington Healthplanfinder to be one of ten Enrollment Centers located in Washington State.