Every year there is a risk of a Medicare or Health Insurance Plan leaving the area. We review and update plans every year. It is one of the reasons that Suzie and Matt go through training every year with Insurance Companies and the Healthplanfinder. Wenatchee Insurance is an independent insurance agency and we contract with different companies to be able to offer options.

Medicare Advantage is my Insurance Plan

You have options to make a change. The first week of October, you will receive the Medicare Annual Notification of Change (ANOC) Letter. Read the letter as it will inform you of price increases and policy changes. If you do not receive a letter then call during those first two weeks of October. Yes, we had a bunch of people ignore their letters one year only to have their Medicare Drug plan drastically increase cost have to wait until the following Annual Enrollment Period to make a change.

The Medicare Annual Enrollment Period is October 15th through December 7th. This is the time period to make changes to Medicare Advantage and Medicare Drug Plans. Yes, we have had people move from a Medigap to an Advantage Plan and this is the time of year to do that.

When your plan is leaving then you get a Special Enrollment Period. (Keep a copy of your ANOC Letter)

You can get a new Medicare Advantage Plan from December 8th to the last Day of February.

You can join a new Medicare Part D Stand Alone plan and you may enroll in a Medigap (Medicare Supplement) within 63 days after your Medicare Advantage Plan ends!

When ever we see a large policy shift, we recommend setting your appointment as early as possible. If you don’t see an appointment then call. We do return calls plus we do our best to expand calendars. Be sure to bring your Red, White and Blue Medicare drug and any prescriptions or Medical information that you want to be checked against your plan.

If you have a PEBB plan or another employer plan then you need to go to them for a review.

Health Insurance is my need.

You have a plan for under 65 then you are probably using the Washington Healthplanfinder. There are some of the lowest cost options available in the area. Matt has been working on these plans so long, he got to test the Healthplanfinder before it went live. A renewal with a connected account and no major changes can take less than 15 minutes. If you have worked with Suzie or Matt over the last two years then you probably have an account connected to them. If you don’t know then give us a call and we can double check prior to the appointment.

Matt got to assist when Premera and Molina left our area and some counties getting down to a single insurance company.

The Open Enrollment for Healthcare is November 1st to January 15th.

When you enroll November 1st to December 15th then your plan starts January 1st.

When you enroll December 16th through January 15th then you plan starts February 1st.

You will want to confirm you plan this year as there are a lot of changes occurring. If you have someone in the Household on Apple Health then you definitely want to understand the updates. If do not see a space available then call the main number. We do our best to find room.

Yes, losing your Health or Medicare plan suddenly can be a shock. Suzie and Matt have seen this hundreds of times and are well prepared for changes. If you have questions then we want to hear them including the middle of the year. We are a full service agency so if you have additional insurance needs then let us know.

As the population of Eastern Washington has continued to grow over the last few years, the availability of work for contractors has steadily grown as well. It has presented a major opportunity for the hustlers and workers who are great at their craft. Whether you have a gift for painting or are excellent at keeping bugs away, the opportunity to get jobs has grown with each new transplant to this state.

Jesse is an expert painter who owns a Moses Lake business and has worked on a lot of remodel projects as a subcontractor while the fixer upper economy has boomed. Despite the fact that Jesse has been working as a painter since he was 18, he had an accident occur at one of his jobs recently. While he was painting on the porch of a flip for a friend of his, he accidentally did substantial damage to the window frame where he was working.

The good news for Jesse is that he had secured General Liability Insurance via Wenatchee Insurance. Many of his fellow painters only carry commercial auto insurance for their trucks. But Jorge realized that even though it wasn’t necessary since his jobs didn’t explicitly require it, having a general liability policy was a way for him to protect both his reputation and his future business. This incident reinforced the potential financial and legal consequences of being uninsured. It highlighted the variety of risks contractors face while working and why having the right types of coverage is important. So what made Jesse decide to buy this additional coverage?

Definition & Importance of General Liability Coverage

General liability is essential liability coverage for Washington contractors. It provides a safety net against third-party claims of injury or property damage. These claims can come from either bodily injury or property damage to people, places, or things that are not part of your business. If your damage is extensive enough, a third-party lawsuit could bankrupt your future. Given that contractors in Washington require a license, insurance and registering with Labor and Industries, it is good to have a plan in place with agents you can work with. Having this relatively affordable coverage ensures that your businesses can operate without the constant fear of potentially crippling legal challenges and financial losses.

If you are working a job, whether it is big or small, you always run the risk of a potential lawsuit if you create accidental property damage. It not only helps in managing the expenses associated with repair but also secures the contractor’s financial stability and reputation in the long run making sure that defense costs are covered and any judgements are taken care of. Every contractor benefits from this coverage, particularly those involved in high-risk trades like electrical, plumbing, or construction.

We’ve established that General Liability Insurance will cover risks such as bodily injury, property damage, copyright infringement, reputational harm, and advertising injury. For contractor insurance coverage, the focus is placed directly on the property damage and bodily injury. Your general liability insurance coverage will address the common claims that contractors face. While it does provide coverage for claims of bodily injury of people who are not employed by your business in some capacity, it’s important to realize that it does not cover you or your employees. That requires workers compensation insurance rather than general liability.

Workers Compensation in Washington state is purchased through the state managed program at the Department of Labor & Industries. Labeling your employees as 1099 independent contractors is not enough and they must past a 7-part test.

For contractors, this insurance offers several benefits. While you are working on or bidding for construction projects it provides protection against lawsuits, enhances credibility, and offers peace of mind. With appropriate policy limits in place similar to what Jesse had for his painting business, it becomes easier to bid on jobs and work knowing that any liability claims that might arise will be covered by the insurance company rather than your bank account.

No Requirement, Big Risk: Why General Liability Insurance is a Must for Washington Contractors

General Liability Coverage Types

In Washington, contractors can choose from various types of business insurance coverage. These can include professional liability insurance to protect your work, inland marine insurance to protect tools, and commercial auto policies. Each of these coverage types are tailored to address specific risks associated with small business operations specifically targeted at the work that you do. It’s important for contractors to understand what each coverage entails to ensure they are adequately protected against potential risks and liabilities inherent in their specific field of work. The three main areas that General Liability addresses for contractors are listed below.

Protection Against Bodily Injury Claims

General liability insurance plays a critical role in protecting against bodily injury claims that are brought by people not associated with or affiliated with your construction business. This coverage is essential for contractors as it mitigates the financial impact of accidents that may occur on the job site causing a bystander to become injured. It benefits you by ensuring the contractor is not held personally liable for these incidents. It covers medical expenses and legal fees, which are vital in maintaining the business’s operations during such events.

Protection Against Property Damage Claims

This type of insurance covers potential liabilities that could arise from damage caused during construction activities. Given that damaging the location where you are working is the most likely potential claim, this physical damage coverage is the most important piece of this insurance policy. While it only protects you for accidental damage, mistakes can be expensive and hard to fund. For contractors, understanding how this coverage works is crucial as it protects against claims that could otherwise severely impact their financial stability.

Legal Defense Coverage

Legal Defense Coverage is a key component of general liability insurance for contractors. It offers significant benefits by covering legal expenses and providing relief during stressful legal claims. This coverage is essential in protecting contractors from the high costs and reputational damage that can result from legal disputes. Why would you want to pay these out of pocket when a small premium cost shifts the burden to the insurance company? Our friend Jesse understood this part.

Legal Requirements for Contractors in Washington

Contractors in Washington are required to carry a contractors insurance policy. To register as a Contractor in Washington state, you must have general liability of at least $200,000 in public liability and $50,000 in property or $250,000 in combined single limit. In addition, you need a surety bond of $30,000 for general contractors or $15,000 for specialty.

But remember, many job sites and general contractors demand proof of insurance before allowing your work to commence. Complying with these requirements not only fulfills legal obligations, but carrying a general liability insurance policy can also give contractors a competitive edge in the marketplace since you can immediately produce a certificate of insurance.

Wenatchee Insurance specializes in helping contractors like Jesse protect themselves and their futures with customized insurance plans. Working with an experienced commercial insurance agent ensures that contractors receive the necessary coverage that matches the scope of their work, providing an essential safeguard for their businesses. That customized commercial insurance plan is provided through Wenatchee Insurance Agency.

Apple Health is going through a massive change because of the Big Beautiful Bill that was passed in 2025. Suzie and Matt have been lending a hand with free or low cost health insurance for years in Washington state.

Yes, we will be looking at enhanced verifications in 2027, if you have an Apple Health plan as it comes up for renewal the changes will come into effect. Yes, the Healthcare Authority has shown that it will be thousands of people in our area impacted by the changes.

Starting January 1st, 2027 adults who qualify for Apple Health must meet work requirements. The exemptions are:

Pregnant or in 12-month postpartum period

Under 19

Foster youth or former foster youth under 26

American Indian/Alaska Native (AI/AN) and certain Tribal Populations

Parent, caretaker, or guardian of a child under 14

Household member of SNAP (food assistance) or TANF (cash assistance)

Parent, caretaker, or guardian of an individual with a disablity

Entitled to Medicare Part A or B

Incarcerated or within 90 days post release period

Medically Frail

Alcohol or substance use disorder treatment (AUD/SUD)

Disabled veteran with 100% total disablity

In a short term hardship

To meet the work requirement you must:

Have at least $580 in monthly income (or average $580 per month over a 6 month period)

Enrolls in an Educational program at least half time

Participates in at least 80 hours per month in a work program

Participates in at least 80 hours per month in community service.

or has a combination of 80 hours of work, community service or educational program per month average.

Yes, the verification is moving to twice a year in 2027. At Wenatchee Insurance, we assist in uploading documentation and lend a hand in understanding the enrollment. There will be at times that the client will have to call the Healthcare Authority directly for an eligibility determination or an activation of a WA Pathways policy.

At Wenatchee Insurance we have supported Apple Health without compensation since our beginning. If you have questions or need assistance then let us know and we will lend a hand.

For growers throughout Wenatchee and Central Washington, crop insurance can be one of the most valuable risk management tools available. However, having coverage is only part of the equation. Understanding how your policy works is equally important. Wenatchee Insurance has a convenient office on Mission street makes getting a question answered easy.

Below are five common crop insurance mistakes that growers should avoid.

1. Waiting Too Long to Review Coverage

Many growers focus on insurance only when enrollment deadlines approach. Unfortunately, waiting until the last minute can lead to missed opportunities and rushed decisions.

Annual reviews are important because:

Farm operations change

Acreage may increase or decrease

New crops may be added

Coverage options can evolve over time

Taking time to review your policy each year helps ensure your protection still matches your operation.

2. Focusing Only on Yield Protection

Yield losses are not the only concern for fruit growers.

In many cases, crop quality can directly affect market value. A crop may still be harvested but receive reduced pricing due to damage, disease, or quality issues.

Understanding the differences between available coverage options can help growers better protect their revenue and overall financial stability.

3. Assuming Disaster Assistance Will Be Enough

While government assistance programs may become available after major disasters, they are not designed to replace comprehensive crop insurance protection.

Disaster programs can vary based on funding availability, eligibility requirements, and the type of loss experienced.

Many farmers view crop insurance as a more predictable and dependable component of their risk management plan.

4. Underestimating Weather Risks

Every growing season brings uncertainty.

Even experienced growers can be surprised by:

Late spring freezes

Unexpected hailstorms

Record temperatures

Smoke impacts from regional wildfires

Water-related challenges

Crop insurance helps provide financial protection when weather-related events affect production or revenue.

5. Not Working With a Crop Insurance Specialist

Crop insurance can be complex. Coverage levels, reporting requirements, acreage documentation, and claim procedures all play important roles.

Working with an experienced crop insurance professional can help you:

Understand available coverage options

Meet important deadlines

Maintain proper documentation

Maximize available protections

Avoid costly mistakes

Crop Insurance Is About Long-Term Stability

Successful farming isn’t just about producing a strong crop this season—it’s about maintaining a sustainable operation for years to come.

Crop insurance helps Washington growers manage uncertainty, protect revenue, and make informed decisions with greater confidence.

If you’re growing apples, pears, cherries, or other crops in the Wenatchee area, reviewing your crop insurance strategy regularly can help ensure you’re prepared for whatever the next season may bring.

Wenatchee Insurance is a full service independent insurance Agency. We support a wide variety of insurance products. In addition to Crop, we regularly lend a hand with whole farm, commercial auto, Car, Dental, Health, Home, Medicare and even travel to name a few.

Washington’s agricultural industry plays a critical role in feeding families across the country, and nowhere is that more evident than in the Wenatchee Valley. Known as the Apple Capital of the World, our region’s growers face unique opportunities—and unique risks—every growing season.

From unexpected spring freezes to excessive heat, wildfires, smoke exposure, hailstorms, and pest pressure, a single event can significantly impact both crop yield and crop quality. For many growers, that can mean the difference between a profitable season and a financial setback.

The Increasing Risk of Weather-Related Losses

Growing fruit in Central Washington requires careful planning and significant investment. Long before a crop is harvested, growers have already invested in labor, irrigation, equipment, fertilizers, and pest management.

Unfortunately, weather doesn’t always cooperate.

Some of the most common threats facing Wenatchee-area growers include:

Spring frost and freeze events

Hail damage

Excessive heat

Drought conditions

Smoke exposure from wildfires

Disease and pest outbreaks

Market-related revenue declines

When these events occur, farmers can experience both production losses and reduced crop quality, affecting overall revenue.

How Crop Insurance Helps Protect Your Operation

Crop insurance is designed to provide a financial safety net when covered losses occur. Rather than absorbing the full impact of a poor season, growers can rely on coverage options that help stabilize income and protect the future of their operations.

Depending on the policy selected, crop insurance may help protect against:

Yield losses

Revenue losses

Quality-related reductions

Certain weather-related damages

Natural disasters affecting crop production

Many crop insurance programs are federally supported, making coverage more affordable and accessible for farms of various sizes.

Crop Insurance Isn’t Just for Large Farms

One common misconception is that crop insurance is only beneficial for large commercial operations.

In reality, small and mid-sized growers often need financial protection the most. A single poor harvest can create challenges that ripple into future seasons, making it difficult to cover operating expenses, equipment costs, and family income needs.

Crop insurance can provide peace of mind and help farms continue operating even after an unexpected loss.

Protecting the Next Generation

Many family farms in Washington have been passed down through multiple generations. Protecting the farm today helps ensure it remains viable for future generations tomorrow.

Whether you grow apples, pears, cherries, stone fruit, or other crops, crop insurance can be an important part of a comprehensive risk management strategy.

Learn More About Crop Insurance in Wenatchee

Every farming operation is different. Coverage options, eligibility requirements, and protection levels vary based on the crops you grow and your specific goals.

Working with a knowledgeable crop insurance professional can help you understand your options and choose coverage that aligns with your operation’s needs.

Renting a basement in someone else’s home is very common in Wenatchee, WA. Many renters assume their landlord’s homeowners policy will cover their personal belongings if something like a burst pipe or fire occurs. Unfortunately, that is not the case. This misunderstanding is something the team at Wenatchee Insurance Agency sees far too often, which is why renters insurance is so important.

Does Your Landlord’s Insurance Cover Your Personal Property?

Your landlord’s homeowners insurance policy is designed to protect the structure of the home and the landlord’s personal property. It does not extend coverage to your belongings as a tenant.

Everything you own, including furniture, electronics, clothing, and personal items, would need to be replaced out of your own pocket if they are damaged or destroyed. Washington State has recognized this gap, and beginning in 2027, landlords are required to disclose this limitation in writing within new lease agreements.

Why Basement Rentals in Wenatchee, WA Come with Added Risk

Wenatchee sits in the foothills of the Cascade Mountains, where spring snowmelt can send significant amounts of water downhill quickly. Basement units are located at the lowest point in a home, making them especially vulnerable to flooding and water damage.

When heavy runoff occurs or sewer systems back up, basements are often the first areas affected. In late 2025, parts of Chelan County experienced flooding that primarily impacted basement living spaces. For renters in these units, the risk of water damage is higher than in above-ground apartments.

What Renters Insurance Covers and What It Does Not

Renters insurance typically helps protect your personal belongings from risks such as fire, theft, and vandalism. It also includes liability coverage if someone is injured while visiting your rental, as well as additional living expenses if a covered event forces you to temporarily relocate.

However, standard renters insurance policies usually do not cover damage caused by natural flooding. To protect against flood-related losses, renters in Wenatchee, WA may need a separate flood insurance policy, which can be purchased through private insurers or the National Flood Insurance Program.

Be Prepared Before the Next Flood Event

If you are renting a basement in Wenatchee, WA and do not have renters insurance, you are taking on significant personal risk. Water damage, theft, or unexpected liability claims can all result in major out-of-pocket expenses.

Wenatchee Insurance Agency works with renters to evaluate their coverage needs, explain policy options, and help secure protection tailored to their living situation. Reviewing your renters insurance now can help ensure you are fully prepared before the next spring runoff or unexpected event occurs.

Let’s talk about the million-dollar question: how much does commercial auto insurance cost? Well, not a million dollars, thank goodness. But it can vary, like choosing between a fancy coffee from Little Red’s Espresso or a cup from your coffee maker at home.

The cost depends on several factors. First, there’s the number of vehicles. If you’ve got a fleet of FedEx delivery trucks, like the ones you see hustling from Leavenworth to Omak, you’re going to pay more than if you’re just insuring a single delivery van.

Then there’s the type of vehicle. A slick sports car used for pizza delivery is going to cost more to insure than a modest pickup truck for auto parts. Plus, if your employees are as careful as a herd of buffaloes in a China shop, your claims history might push those premiums up.

The driving records of your employees also play a big part. If your star driver has a clean record, you’re in great shape. But if Bob from accounting keeps getting tickets for speeding through the roundabout near Central Washington University, that’s going to hurt the bottom line.

And don’t forget coverage limits and deductibles. The higher the limit and the lower the deductible, the more you’re going to pay. It’s like deciding between getting an extra scoop of ice cream with sprinkles or sticking with the single – more coverage costs more.

So, on average, you might pay around $147 to $188 per month per vehicle. But just like with everything in life, we shop around and compare.

It’s like finding the best apple at the market – you’ve got to look around to get the best deal. As an independent insurance agency, we work with multiple companies to find our clients good rates in Washington state.

Just think of Wenatchee Insurance as your trusty sidekick, ready to jump in and save the day when things go awry.

Topics: Progressive, Commercial Auto, company car, collision coverage, collision coverage, delivery, Wenatchee Insurance, Chelan County, Grant County, Douglas County, Okanogan,

Beginning June 11, Washington state has made a major change around your E-Bike. Washington state recently updated its laws through Enhanced Substitute Senate Bill (ESSB) 6110 to better define the difference between electric-assisted bicycles (e-bikes) and electric motorcycles. With new technology, we see an update of laws.

In 2013, Washington state allowed for Electronic Proof of insurance. In 2019, we saw Washington State require motorcycles to be insured. As the laws change in Washington state, Wenatchee Insurance will be ready.

If your E-Bike has:

Fully operational Pedals

Has an electric motor rated at 750 watts or less.

Can not exceed 20 mph on electric motor alone.

then your E-Bike is still considered an E-Bike.

If it does not meet those standards then it is considered a motorcycle and you may have additional requirements like:

Motorcycle Helmet means means a protective covering for the head consisting of a hard outer shell, padding adjacent to and inside the outer shell, and a neck or chin strap type retention system, with the manufacturer’s certification for the Department of Transportation. Be aware of unsafe or novelty helmets.

To be insured in Washington state you must carry a minimum liability of:

$25,000 for injuries or death to another person

$50,000 for injuries or death to all other people

$10,000 for damage to another person’s property.

Wenatchee Insurance is an independent insurance agency that has multiple companies to insure E-bikes or Motorcycles. If you would like assistance then let us know.

If you frequently travel in your RV to and from Wenatchee, WA, it may feel more like a primary residence than a vacation vehicle. Choosing the right RV insurance depends on how often you use your RV and whether it serves as your primary living space. The professionals at Wenatchee Insurance Agency can help you determine whether part-time or full-time RV insurance best fits your lifestyle.

RV Insurance for Recreational and Part-Time Use

Recreational RV insurance is designed for people who use their RV primarily for vacations, weekend trips, or seasonal travel. These policies function similarly to an auto insurance policy and focus on collision and comprehensive coverage while the RV is on the road.

Many recreational RV policies also include vacation liability coverage, which applies when your RV is parked at a campsite. Limited personal property coverage is typically included as well, often ranging from $1,000 to $3,000. This amount is usually sufficient for clothing, small electronics, and basic travel gear.

When Full-Time RV Insurance Is Required

Full-time RV insurance is intended for individuals who live in their RV for at least 183 days per year or who do not maintain another primary residence. These policies combine elements of auto and homeowners insurance to provide broader protection.

Common features of full-time RV insurance may include:

Full-timer personal liability coverage that extends beyond campground use

Loss of use coverage if your RV becomes uninhabitable due to a covered loss

Medical payments coverage for injuries to others

Higher personal property limits, often $20,000 or more

Snowbirds who spend several months traveling seasonally and digital nomads who live and work year-round in their RVs typically need full-time coverage. If your usage does not match the policy you carry, your insurer may deny claims.

Understanding which RV insurance policy you need is essential to protecting both your vehicle and your lifestyle. Contact the professionals at Wenatchee Insurance Agency, proudly serving Wenatchee, WA, to learn more about part-time and full-time RV insurance options.

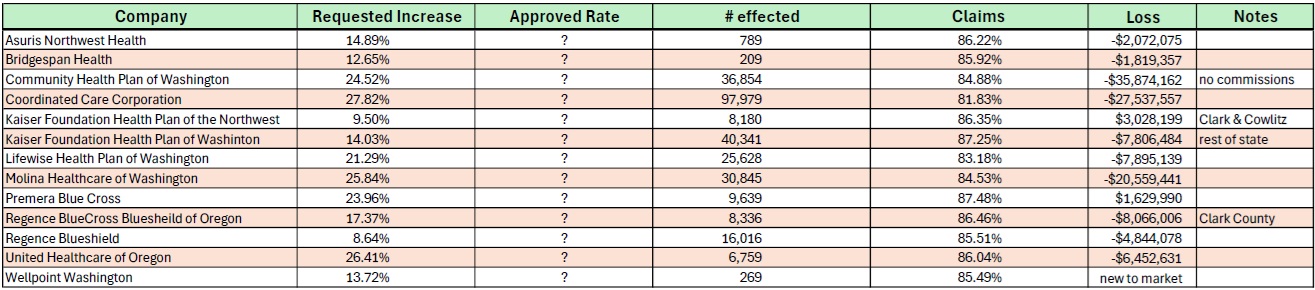

The Office of the Insurance Commissioner has released the proposed individual rates for 2027. A consumer can even comment about the proposals on the OIC’s Webpage. It’s a very good idea to give feedback. Last year we saw a massive jump in rates and we are seeing a repeat with the lack of positive legislation.

The loss of the Enhanced Tax credits has drove the uninsured number higher which costs to providers who pass on the cost to the consumer. These impact rural families, small businesses and early retirees the most. It directly impacts millions of Americans.

The Medical Loss Ratio. A individual insurance company must spend at least 80% of premiums on healthcare or they rebate the owner of the policy. There isn’t a single insurance company that was under 80%. For a successful change to occur then Provider and Pharmaceutical prices have got to be addressed.

These are not the final rates. The average requested rate is 22.4% and individual plans could shift very differently that the overall picture. They have to be approved by the Office of Insurance then approved by the Healthplanfinder.

There are plans that are choosing to de-commission so consumers will have fewer options for customer service. The more plans that offer fewer commissions, it makes it a challenge to keep lights on for community resources. Some agents may drop out or start charging fees. We do our best to offer additional types of insurance to fill in the gaps and allow our health agents to continue despite an Insurance company failing to compensate.

For nearly a decade we have assisted with Health & Medicare Solutions. We are proud to be selected by the Washington Healthplanfinder to be one of ten Enrollment Centers located in Washington State.