OK, here is your quick lesson that Chat GPT won’t tell you about Life Insurance.

I had a client Message me the other day saying that they they, “wanted Guaranteed Issue Life Insurance” because they are not going to get conventional life insurance. They they included a screenshot with some telltale signs they were reading from a script that AI had produced for them.

AI was queuing up on a marketing terms and not providing the necessary details that had limitations and how a policy worked. We are still in the early stages of AI. It can provide you great driving directions to get to the baseball field but it won’t play the game for you. That is where an agent comes into play to provide the coaching necessary for a good selection.

What the client’s AI was failing to mention was they will still reference your medical records and do a questionnaires for policies that don’t have a physical examination. All Life Insurance goes through some sort of underwriting. Some are a lot less than others.

To solve the problems, I went looking at the No Physical Exams Policies underwriting guidelines and they all contained looking at Medical Records. Yes, the Medical Information Bureau (or MIB) is a real thing for Life Insurance. You would have to know what was in your file if you wanted to work with one of those policies.

The one with the fewest questions and the fewest review for Medical Records that we have access to is called Final Expense. You must be 45 or older to start a policy. They won’t start them earlier.

You can play on my quoter and look to see if I missed one with easy underwriting. Or give our office a call and we will walk you through options that you might not know existed.

Tax season is almost here and people start looking for their 1095 form. It runs from January 16th through April 15th of 2026. If you are receiving your healthcare from the Washington Healthplanfinder, you must file your taxes. It is how the Federal Government double checks if you are receiving all of the help that you are qualified for in the form of Advanced Premium Tax Credits that lower the monthly cost of insurance.

If you receive too much APTC then you will have to repay some or all the excess amount when you file your taxes.

If you receive too little APTC then it will increase your tax refund or lower the amount of taxes that you owe.

There are 3 types of 1095 form

1095-A form is made available usually in the last week of January on the Healthplanfinder and a copy is mailed out. This is for the people who were receiving tax credits that the reduce of the cost of healthcare. In our immediate area in Central Washington if you have Ambetter, Community Health (paid plan) or Lifewise then you will have one of these forms.

If you don’t have a printer and need a copy if you are a client and stop at Wenatchee Insurance on Mission Street, then we can print an additional copy for you.

1095-B form is for the people using Apple Health. It is provided by the Healthcare Authority. It is not mailed out. You can request a form directly from the Healthcare Authority’s page. Form 1095-B is not required when filing taxes.

1095-C form is from employer sponsored health insurance. It is not required for filing taxes.

The 1095-A Form is needed to fill out Form 8962 to reconcile. We saw clients in 2025 that failed to properly file this have problems with their tax credits and recommend filling on time with all forms to prevent the loss of tax credits.

Remember you can adjust your income through the year to better reflect your income so that you don’t have to pay back excess tax credits.

Suzie and Matt have been lending a hand for 13 years in better understanding Health Insurance and if you have questions or just want someone to double check your account it is easy to add a broker of record.

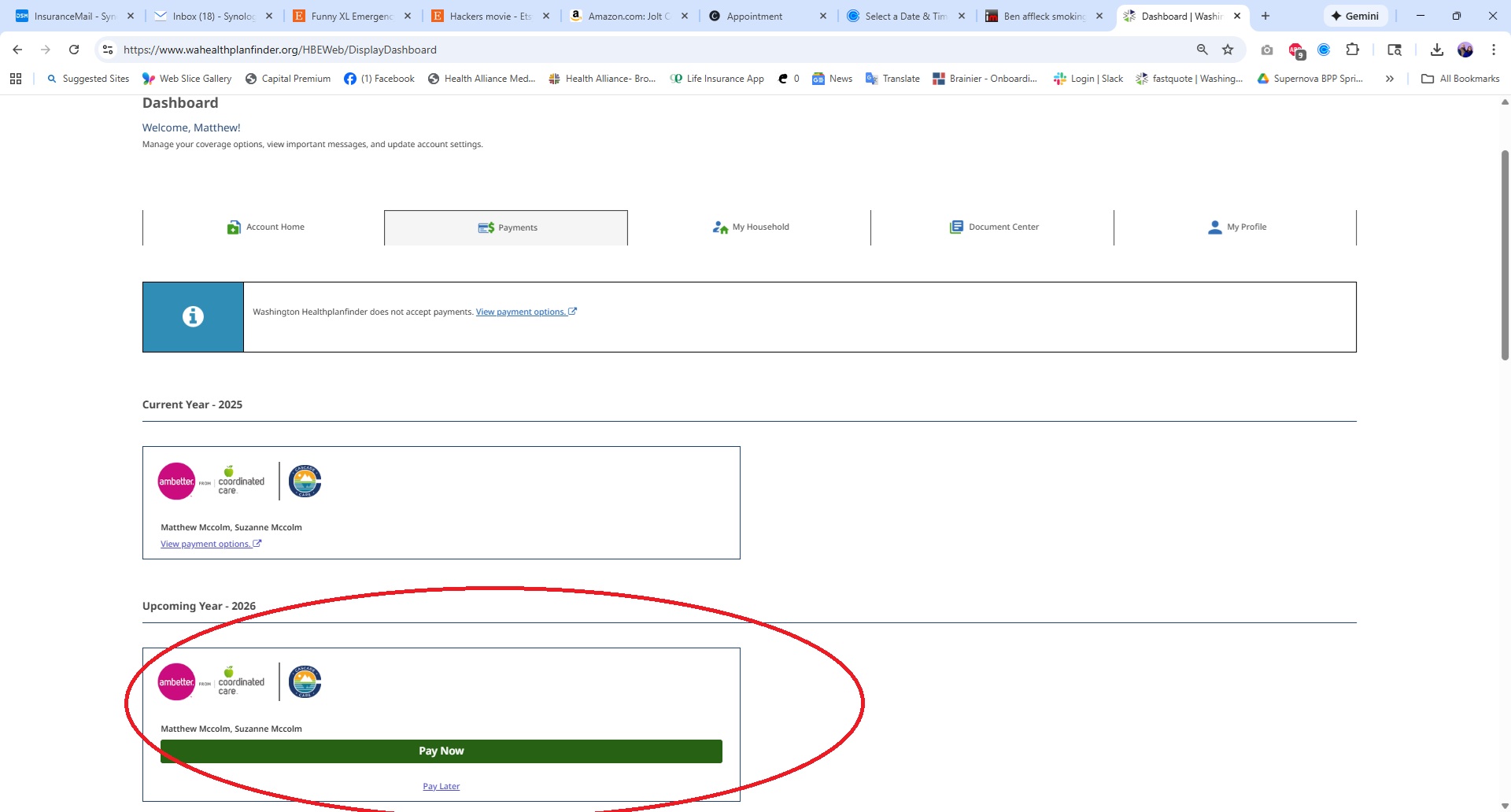

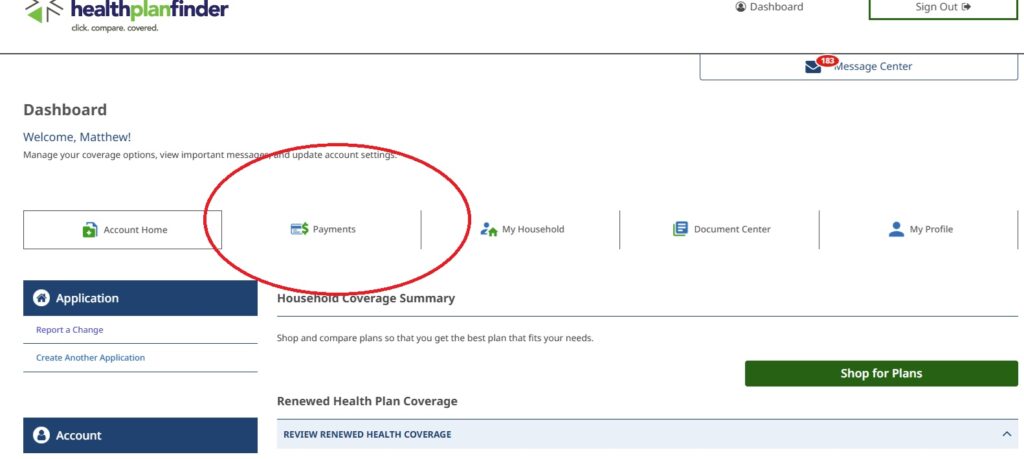

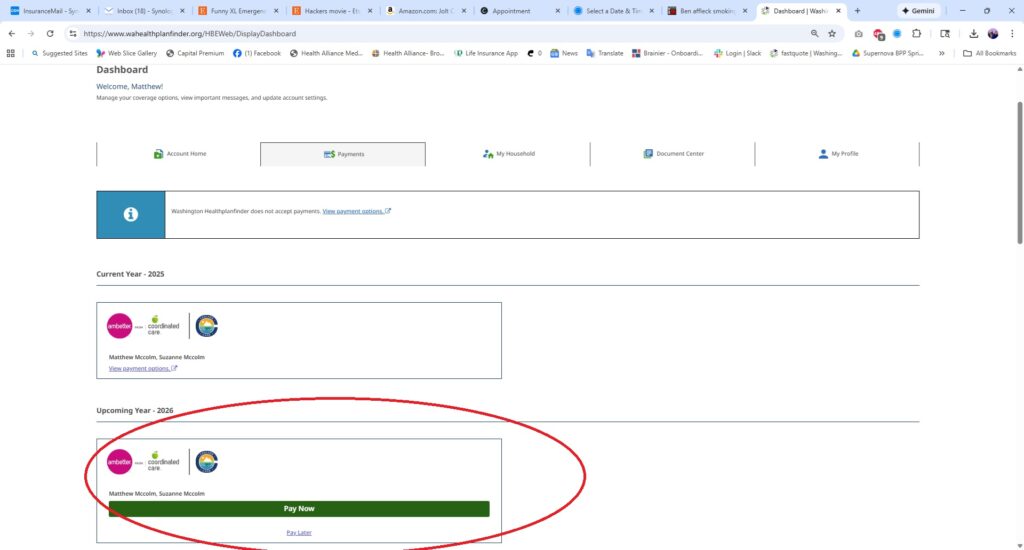

We help a lot of people in Washington State with their enrollment and education about health insurance. If you are using the Washington Healthplanfinder during Open Enrollment then you have a pay now button feature to get the initial payment completed. We are brokers and don’t charge fees for our work.

When you log into the desktop version. You will see a row of buttons across the top. You want the one labeled Payments.

During most of the year, the payment tab will list payment options. However during Open Enrollment, the Washington Healthplanfinder will list a pay now button for most companies. When you click on the pay now button for it will create a pop up which goes to a secure payment site for the company.

This first payment is important as it secures the insurance policy. Most companies wil then send the policy’s insurance cards and information booklet after this payment has been made. A few of the companies will allow you to schedule monthly payments using the popup while others you will have to set up with them at a later time. The booklets and cards usually arrive about two weeks after the payment.

At Wenatchee Insurance Agency, Matt and Suzie have been lending a hand to our community for over 13 years with Health Insurance. While our agency does a whole lot more, we get asked a lot of questions regarding Health because it is complicated.

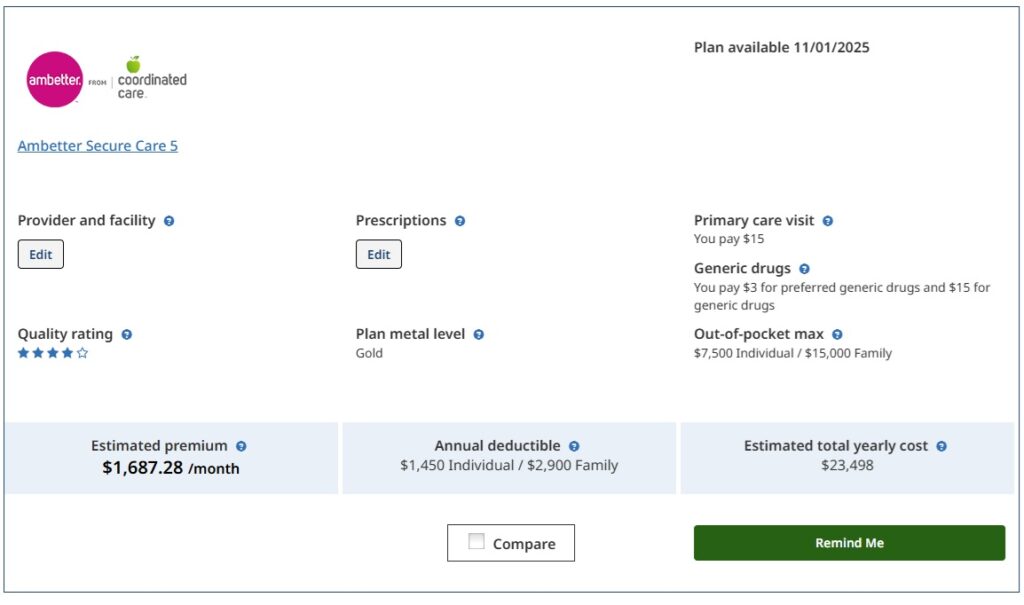

The 2026 rates have been approved and are visible for the first time on the Washington Healthplanfinder. As I write this post the Silver plans were not loaded and you can not compare them side by side with your 2025 plans. All of the 2026 plans are listed on the Office of the Insurance Commissioner.

2026 rates first look

This is off the main screen from the Washington Healthplanfinder. It is only an estimate. It can change depending on what Congress does regarding the enhanced tax credits and the Healthplanfinder. When the enhanced tax credits were introduced, the first month that they went into effect was June of 2021. It made quite a difference in keeping money in the pocket’s of American households.

Our household is no longer eligible for tax credits with the current plan from Congress. So we have to make the jump from a couple hundred dollars to approaching $1687 per month. As small business owners, we don’t have the luxury of a large group plan. It will be about 1/4 of our income for 2026 before we get into use.

The Health Open Enrollment Period is important to talk about. The plans have made some big shifts and if you are eligible for tax credits will be more manageable. It is important to talk with someone who has a greater understanding of insurance than “that Uncle” eight into a case at Thanksgiving.

November 1st through December 15 for health plans starting January 1st

December 16 through January 15th for health plans starting February 1st.

Medicare has it’s own enrollment periods and there are special enrollments. We run applications year round just in case we find a Special Enrollment that works or to prepare for the next open enrollment.

Every year it is important to look at your plan because of changes. There are times that plans do not automatically renew or need to be updated. If a plan leaves the area then you may have been moved over to a plan that doesn’t work as well.

At Wenatchee Insurance Agency, we like to review plans every year during the Open Enrollment Period. This is Matt’s 13th Open Enrollment. We walk through all the plans available. We do not charge broker fees and if any commission is available it comes from the insurance company.

Beginning January 1st, 2026 some medical procedures under traditional Medicare will require Prior Authorization in six states before performing the service. Yes, Washington state has been selected. Arizona, New Jersey, Ohio, Oklahoma, and Texas.

This updates individuals with Medigap plans such as Plan G or Plan N, if they are using traditional Medicare coverages. While common in health plans and Medicare Advantage Plans these are new for original Medicare.

What Procedures will require a Prior Authorization?

There were 17 types of procedures that were flagged to now need approval. Here is what made the list.

Facet joint procedures for back pain

Nerve and muscle tests (electrodiagnostic testing)

TENS units and similar electrical stimulation devices

Hyperbaric oxygen therapy

Spinal cord stimulators

Deep brain stimulation (commonly for Parkinson’s)

Sacral neuromodulation (for urinary conditions)

Transcatheter aortic valve replacement (TAVR)

Arthroscopic knee cleaning or debridement

Vertebroplasty/kyphoplasty for spine fractures

Epidural steroid injections

Non-emergency ambulance transport

Botox injections for medical issues

Negative pressure wound therapy pumps

Hernia repairs

Lumbar spinal fusion

Skin graft substitutes for chronic wounds

Physicians will be required to submit documentation before the service is performed. If approval is not granted, coverage can be denied requiring the patient to pay out of pocket.

At Wenatchee Insurance we do our best to lend a hand in understanding and enrolling in Medicare and insurance Programs. We are an independent insurance agency. If you are looking at supplemental policies then let us know and there are enrollment periods.

OK, Tariffs are playing an important role in what the administration is doing with drug pricing. TrumpRX appears to be using them to inflate the price on medication for companies that don’t participate with the administration.

Trump is imposing a 100% Tariffs. Effective October 1st, 2025 if a company reaches an agreement with the Administration then they will be immune to them. There is the common consensus that everyone participating in this deal will have customers paying inflated costs due to the tariffs.

Companies working with TrumpRX

Pfizer is one of the first companies to reach an agreement. They are one of the largest drug companies and Eliquis, Ibrance and the Covid vaccine are among the drugs that they manufacture. Eliquis was one of the drugs with the Medicare Negotiated price for 2026. Ibrance was selected for the Inflation Reduction Acts Medicare negotiated price for 2027. So thanks to the Inflation Reduction Act from the Biden administration,

They will be doing a Direct to Consumer Model with a yet to be launched website. There is a marked page at TrumpRX.com but it is not functional as of publishing this blog.

It could be very similar in the direct to consumer model of AmericasMedicines.com from a Pharmaceutical trade group PhRMA where people can go directly to the manufacturers.

It sounds like a stepped up version of Mark Cuban’s CostPlus. Where they have a few drugs that they ship directly to the consumer.

Only time will tell if it has more savings than GoodRX.

Important Dates for Medicare and Health

Medicare Advantage and Prescription plans can be enrolled or changed October 15 through December 7th.

Healthcare Plans can be enrolled or changed November 1st through December 15th.

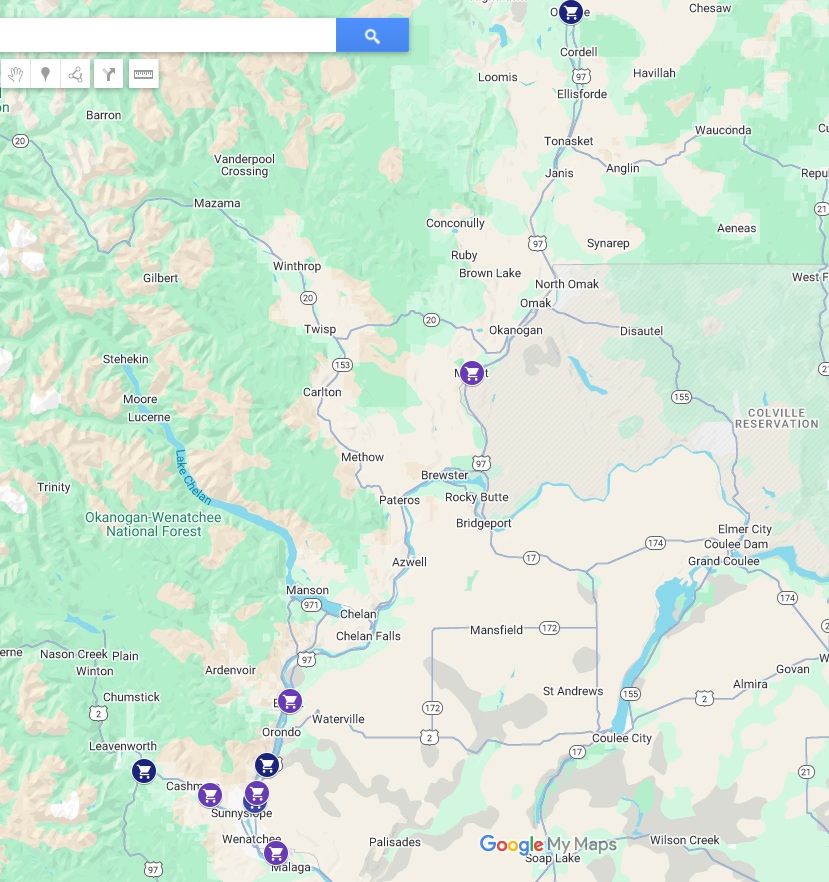

Since Wenatchee Insurance is located in the Apple Capital of the World, we do our best to meet the Orchards and small businesses in our area. One of the ways that we are able to is by visiting their fruit stand during harvest. We do our best to carry cash to lower transaction fees. If you want fresh fruits & vegetables while putting money directly into farmers hands then this is one of the best ways to do it.

While there are some very large tourist driven stands, we have been doing our best to visit the smaller operations. Some of these we have been visiting 20 plus years while others it has been our first stop. We are doing farm house rules by purchasing something fresh and something preserved.

Eagle Rock Fruit Stand: address 4911 Selfs Motel Rd, Cashmere, WA 98815 : Phone: (509) 470-6292 Facebook Page; Just did their 20th Anniversary. One of the most affordable that we found for cherries.

The Peachman (formerly Tonz Ochards): address is 4820 Cascade Ln, East Wenatchee, WA 98802: Phone (509) 630-4674 Facebook Page One of the few places where we were able to find Pie Cherries. They had a great selection of pickled goods. We pulled a bottle of Peach syrup out of here.

Miller Orchards: address is 7306 US-97, Peshastin, WA 98847 : phone (509) 669-3784 Facebook Page Yes, this is where Matt can find his Santini Cherries. They have very high quality produce and we were able to get some amazing blueberries from here as well.

Lake Entiat Fruit stand: address 14360 US-97 ALT, Entiat, WA 98822 ; phone number (509) 393-0539 websiteFacebook We had some amazing strawberries out of here. Seriously, our car smelled delightful from the ride home. Matt also picked up marinated mushrooms which is hard to find.

Homestead Fruit Stand: address 7920 State Highway 97A, Wenatchee, WA 98801; phone number (509) 665-8243. They had some great produce and we were able to pull some ripe tomatoes. This is the first stand into Entiat from Wenatchee. They had a good selection of Lavender.

DeLap Fruit Stand: addressmilepost 275 Hwy 97 Malott, WA, United States, Washington 98829; phone number (509) 422-3145; Facebook page; They have some fruit that you may not have had before. You can find Apruims and Pluots. They have one of the dancing guys and are an easy stop off Hwy 97.

Estes Fruit Stand and Flowers: address 13656 US-2, East Wenatchee, WA 98802; phone (509)884-2034; Facebook page ; This was one of my mother’s favorites. They have this amazing flower selection and this was the earliest that that I spotted this year’s apples as they had some early varieties.

E & E Fruit Shack; address 4th St SE, East Wenatchee, 98802. There is no website or Facebook page. It is however right next to the family’s orchard. We were able to pick up some great plums, they also had peaches, and a bunch of zucchini. If you want to put money directly into a farmer’s hands then this is where you want to pick up fruit here at least once during the season.

Feil Pioneer Fruit Stand: 13083 US-2; East Wenatchee, WA 98802. Phone number 509-669-1754. This is right on the highway next to the round about. Great selection of fresh fruit. The earliest spot that we found Pears and Apples. They even had a great selection of tomatoes.

Prey’s Fruit Barn: 110007 Hwy 2, Leavenworth. Phone number 509-548-5771. Facebook pagewebpage This is right outside of Leavenworth with the large American Flag. They had a good assortment of fruit and are open year round. Very tourist friendly and we were able to pick up unusual sodas.

Bonus: The Local Granola: address 1408 Main Street Oroville, WA, United States, Washington 98844; phone number (509) 476-7037; webpageFacebook They offer a small natural foods selection. The Granola is worth the stop. We also got beard supplies.

Rules for fruit stand visits.

Bring cash. The smaller operations will appreciate you as they don’t have to make transaction fees.

Don’t be afraid to call ahead or ask if you don’t see something. It’s literally how I got Pie Cherries.

When you find one that is awesome then take a picture and share them on Facebook. Bonus points if you tag them so that more people can find them.

If we missed a favorite one then let us know in the comments.

At Wenatchee Insurance, we lend a hand to farms and orchards with a wide background. Insuring your family business can be tricky and adding crop insurance requires some skills. Some folks are looking for a Multi- Peril Crop Insurance where others are needing Whole Farm Revenue Protection. Living in the Apple Capital of the World, we have have run between the trees more than once.

We will ask questions so that we can get a better picture about your orchard or farm to make sure that you are not creating a coverage gap. For us, we believe that insurance should be:

Affordable. If you can not pay for it then it doesn’t make sense.

Understandable. This creates big problems if someone has something that they don’t know how it works.

Useable. If an emergency arises then we want you to be able to use it.

Crop insurance questions

What is the address of your orchard or farm?

What is the name of the orchard or farm?

Who has an interest in the orchard beyond yourself?

What is your and any other people with interest’s SSN?

What is the business’ EIN (If individual SSN or RAN is fine)

Are you leasing the orchard?

If so what is the % agreement?

What fruit or crop are you growing?

How many acres do you have of which crop?

What are the last 5 years of production? We will need it by block if possible

If new farmer can you procure the previous farmer’s records?

Are you tearing out any part of your orchard for next year? Or is there any new tree you think will produce this year?

Anything you think I should know?

What’s next to insure your crops?

After collecting the information, we go looking for coverage that covers your needs. What works for Farmer Fred’s potatoes in Quincy may completely miss Oliver Pear Orchard in Cashmere. Not everyone needs or can get crop insurance. We do our best to be responsive whether it is you talking or if you are sending your spouse.

When you are ready let’s talk. We have found that a conversation is a great way to begin.

At Wenatchee Insurance, we lend a hand to business owners with a wide background. Business insurance can be tricky. Some are just starting their journey where some have been running their family business for five generations. We even got involved with lending a hand with assisting Enterprise For Equity to help people better insure their business.

We will ask questions so that we can get a better picture about your business to make sure that you are not creating a coverage gap. For us, we believe that insurance should be:

Affordable. If you can not pay for it then it doesn’t make sense.

Understandable. This creates big problems if someone has something that they don’t know how it works.

Useable. If an emergency arises then we want you to be able to use it.

Retail business insurance questions

1) What is the official name of your business?

2) What is the address where you operate? Is it online only home based?

3) Do you have a different mailing address? If so What?

4) What is a your business phone #?

5) How much do you think you’re going to be making this year?

6) Does anyone else own a stake in the business?

7) Do you use your car to make deliveries?

8) What is the product/s you sell?

9) How many employees will you have?

10) Are there any additional insureds? (Landlords/owners)

11) Anything you think I should know?

What’s next to insure your business?

After collecting the information, we go looking for a good insurance company that fits your business. Some insurance companies may charge more or even not cover something that you need. What works for Farmer Fred in Quincy may completely miss Oliver Orchard in Cashmere. Not everyone needs crop insurance. The old company that your grandfather used may not cover the drones that you are using today.

When you are ready let’s talk. We have found that a conversation is a great way to begin.

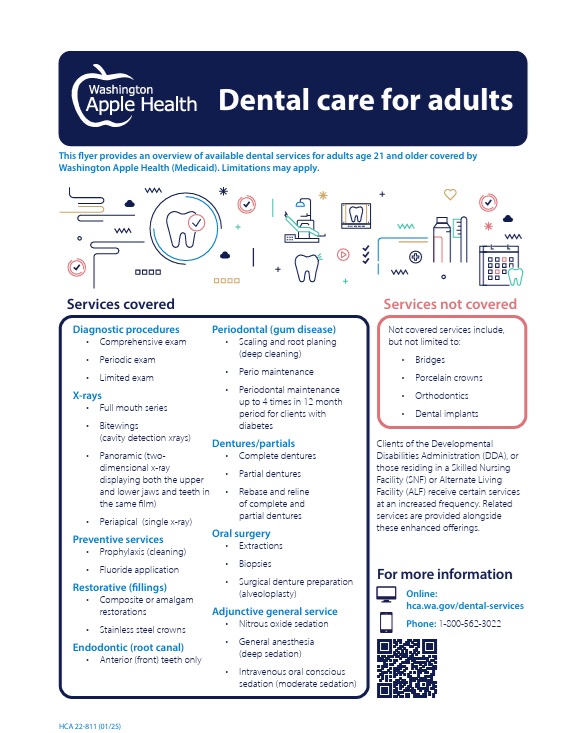

In our area we have a select few dentists and orthodontists that accept Apple Health. When our son needed braces, every six weeks we would make the drive from Wenatchee to Ellensburg so that he would have his teeth worked on. It took a lot of coordination between his pediatric dentist and the orthodontist to get the approval.

Where to find Apple Health Dental care?

OK, have you been to the Dentist Link Set up by the Healthcare Authority? It provides an excellent search tool to find a dentist accepting Apple Health Dental in your area. You can also call or test a referral specialist 844-888-5465 from 8 am to 4:30 pm on weekdays.

What does Apple Health Dental cover for adults?

If you have Apple Health as an adult it covers more than people think. Yes, it really does take care of fillings, front teeth root canals and dentures. There are some things that it doesn’t cover by it’s self like Dental Implants and Adult Orthodontics.

How do I enroll?

Suzie and Matt have been assisting people enroll for over a decade into Apple Health plans. We have never charged a fee and do not get paid for enrolling people in these plans. We do it because people in our community use healthcare and it is expensive to go without. There are no enrollment periods with Apple Health and it is based on our income level.

Children have expanded access to Apple Health using the Children’s Health Insurance Program (CHIP). Some will be zero cost or there will be a $20 or $30 monthly charge per child fee. We have a lot of families where the parents are on a paid health plan and the kids are on Apple Health. The important thing is that the family is being covered.

What happens if I am no longer eligible for Apple Health Dental

We have the conversation. We have access to several dental plans that a person can enroll year round. Some with waiting periods and some without. We even have plan that can assist adults with getting braces after a waiting period at Wenatchee Insurance. We make it as easy as possible to review your options.

There are times when it get’s incredibly busy for healthcare so you may have to wait a little bit longer in the Fall.

For Medicare the Annual Enrollment Period for Medicare Drug Plans and Medicare Advantage plans is October 15th through December 7th.

For Medicare’s Initial Enrollment it is three months before you turn 65, the month of your birthday and three months after.

For Healthcare the Open Enrollment Period is November 1st through December 15th. (some states may have an extension so do not hesitate to ask).

Yes, people set appointments early in the year for fall appointments to insure that they are able to have a conversation about the changes to their health plan.

For nearly a decade we have assisted with Health & Medicare Solutions. We are proud to be selected by the Washington Healthplanfinder to be one of ten Enrollment Centers located in Washington State.