Help, my Health Insurance Plan (or Medicare Plan) is leaving

Every year there is a risk of a Medicare or Health Insurance Plan leaving the area. We review and update plans every year. It is one of the reasons that Suzie and Matt go through training every year with Insurance Companies and the Healthplanfinder. Wenatchee Insurance is an independent insurance agency and we contract with different companies to be able to offer options.

Medicare Advantage is my Insurance Plan

You have options to make a change. The first week of October, you will receive the Medicare Annual Notification of Change (ANOC) Letter. Read the letter as it will inform you of price increases and policy changes. If you do not receive a letter then call during those first two weeks of October. Yes, we had a bunch of people ignore their letters one year only to have their Medicare Drug plan drastically increase cost have to wait until the following Annual Enrollment Period to make a change.

- The Medicare Annual Enrollment Period is October 15th through December 7th. This is the time period to make changes to Medicare Advantage and Medicare Drug Plans. Yes, we have had people move from a Medigap to an Advantage Plan and this is the time of year to do that.

- The Medicare Advantage Open Enrollment Period is January 1st – March 31st. You are allowed to make one change to a Medicare Advantage Plan during this time frame.

- When your plan is leaving then you get a Special Enrollment Period. (Keep a copy of your ANOC Letter)

- You can get a new Medicare Advantage Plan from December 8th to the last Day of February.

- You can join a new Medicare Part D Stand Alone plan and you may enroll in a Medigap (Medicare Supplement) within 63 days after your Medicare Advantage Plan ends!

We have gone through this process when Sound Path Health and Health Alliance left the area. Suzie is very good at smoothing out the differences between the old and new plans.

When ever we see a large policy shift, we recommend setting your appointment as early as possible. If you don’t see an appointment then call. We do return calls plus we do our best to expand calendars. Be sure to bring your Red, White and Blue Medicare drug and any prescriptions or Medical information that you want to be checked against your plan.

If you have a PEBB plan or another employer plan then you need to go to them for a review.

Health Insurance is my need.

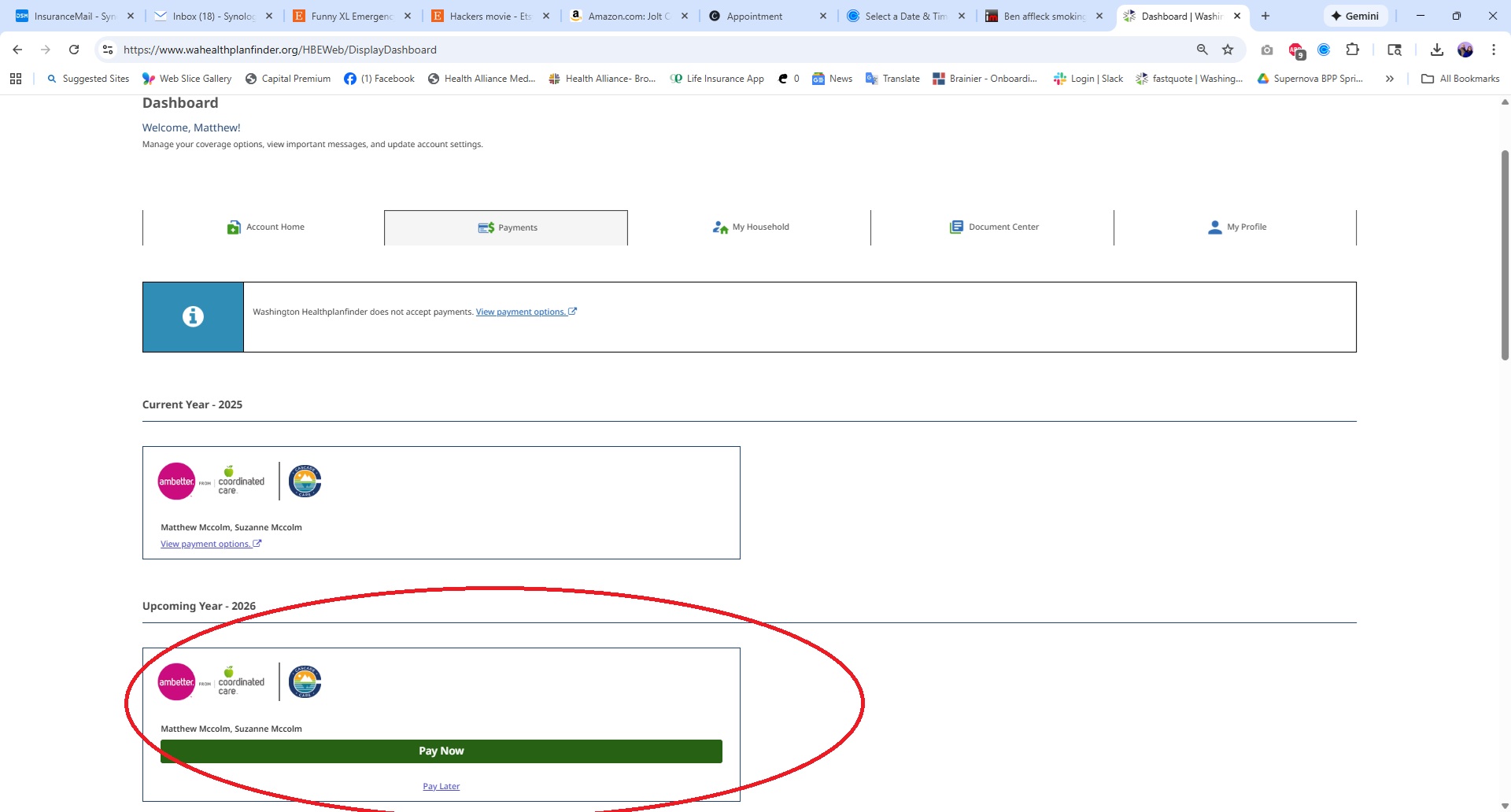

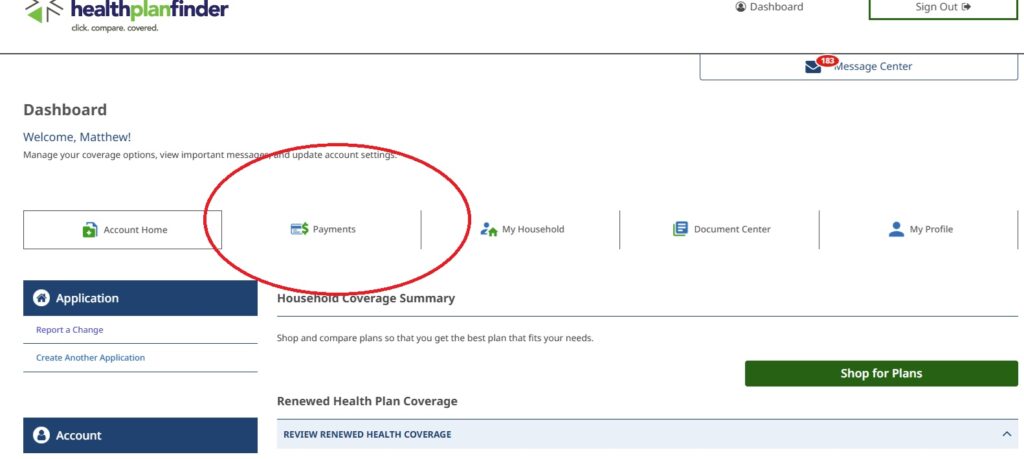

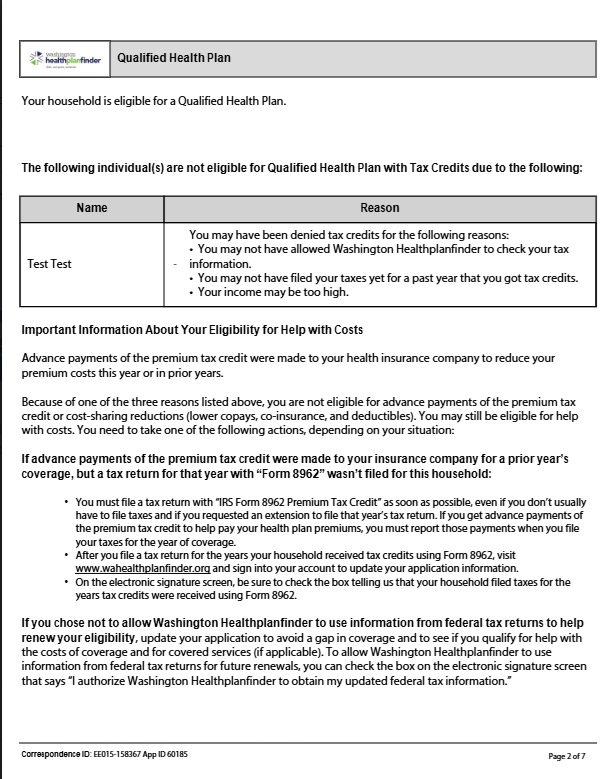

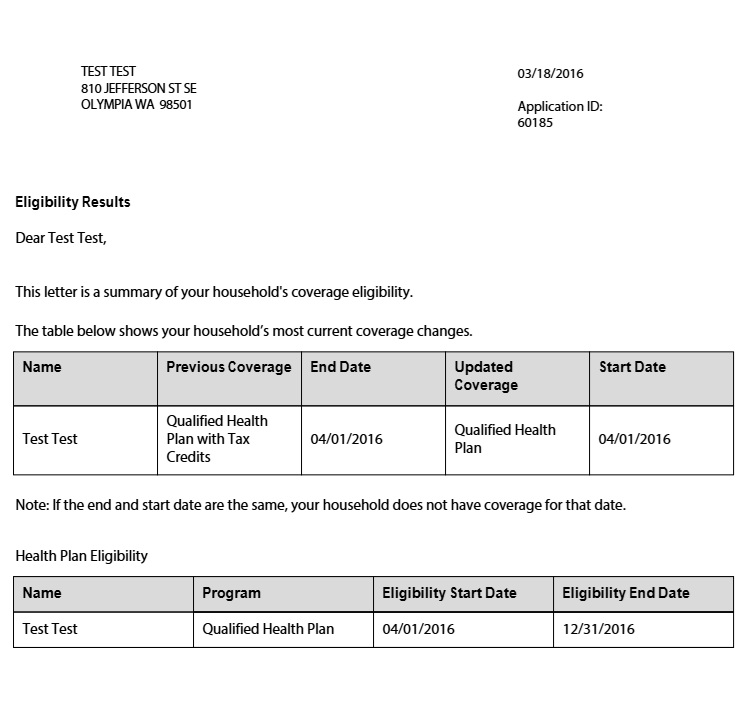

You have a plan for under 65 then you are probably using the Washington Healthplanfinder. There are some of the lowest cost options available in the area. Matt has been working on these plans so long, he got to test the Healthplanfinder before it went live. A renewal with a connected account and no major changes can take less than 15 minutes. If you have worked with Suzie or Matt over the last two years then you probably have an account connected to them. If you don’t know then give us a call and we can double check prior to the appointment.

Matt got to assist when Premera and Molina left our area and some counties getting down to a single insurance company.

The Open Enrollment for Healthcare is November 1st to January 15th.

When you enroll November 1st to December 15th then your plan starts January 1st.

When you enroll December 16th through January 15th then you plan starts February 1st.

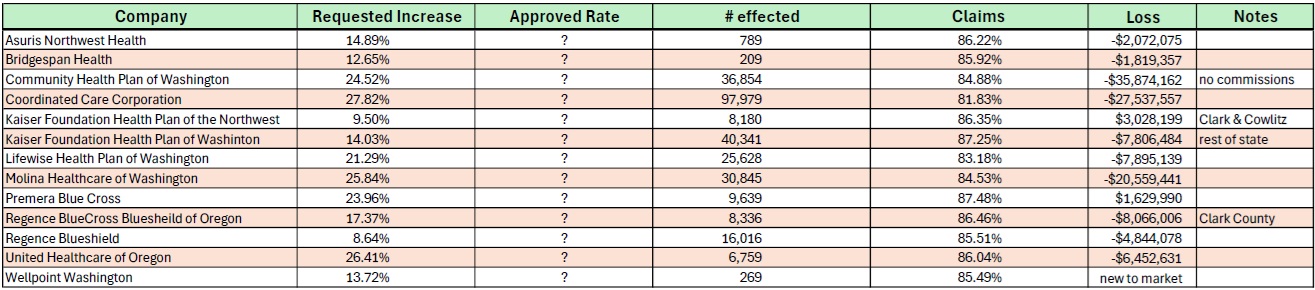

You will want to confirm you plan this year as there are a lot of changes occurring. If you have someone in the Household on Apple Health then you definitely want to understand the updates. If do not see a space available then call the main number. We do our best to find room.

Yes, losing your Health or Medicare plan suddenly can be a shock. Suzie and Matt have seen this hundreds of times and are well prepared for changes. If you have questions then we want to hear them including the middle of the year. We are a full service agency so if you have additional insurance needs then let us know.