You run a high-risk business in Wenatchee, WA, but aren’t sure if you need umbrella insurance or not. We at Wenatchee Insurance Agency can tell you that you absolutely do! There are many reasons why this policy type is so important, so please read on to learn more about why.

Umbrella insurance is an overarching protection policy (hence its name) that expands your liability. It’s usually chosen by businesses that want to avoid expensive liability costs. When used properly, it can minimize the danger of expensive lawsuits and improve your financial situation.

Typically, your policy comes into play the moment you max out your liability coverage. For example, let’s say you pay your total liability out to help someone after an injury. Instead of paying out of your pocket, your umbrella protection will kick in and pay the rest of the costs (up to a certain limit).

How Does It Help You?

If you have an umbrella insurance policy, your liability protection for your high-risk business is significantly increased. Let’s say you run a hunting company, and someone gets shot by accident on a trip. With umbrella insurance, you can pay for their recovery without worrying about maxing out your policy.

Furthermore, you can even use your umbrella insurance as an advertising tool or as a way of mitigating your company’s risk. It might even improve your value or decrease your insurance price, depending on a myriad of factors. That makes umbrella insurance essential.

Who Can You Call?

If you live in Wenatchee, WA and want to work with an insurance provider you can trust, call us at Wenatchee Insurance Agency. We’ll talk with you about your policy, discuss potential upgrades to your coverage, and make sure that you get the high-quality help that you need to stay strong.

You need insurance coverages for the wind, snow and ice. Between Blewett, Snoqualmie Pass and the Vantage Bridge, the roads can get rough. Let’s sprinkle in some winter-themed humor with snow and ice into our semi truck insurance coverage list for your trucking business that we should talk about.

Primary Liability Insurance: From Wenatchee Insurance Agency, it’s like giving your truck a superhero cape, but with extra padding for those slippery snowball fights on the highway.

Physical Damage Coverage for Icy Encounters: This is like kitting your truck out in a snowsuit. Perfect for those chilly days when your truck decides to go ice skating across the road.

Cargo Insurance for a Winter Wonderland: Whether you’re hauling apples or timber, Wenatchee Insurance Agency has you covered like a warm, fluffy snow blanket on a cold winter night.

Bobtail Insurance for Snowy Solos: Ideal for when your truck wants to make snow angels on its day off, ensuring it can frolic in the winter wonderland without a worry.

Uninsured/Underinsured Motorist Coverage with a Frosty Flair: It’s like having a friendly yeti guarding your truck against drivers who think insurance is as mythical as a snow dragon.

General Liability Insurance for Slippery Situations: Watch out for those ice patches! This coverage is like having a team of penguins on standby to guide anyone who might slip on an icy patch at your business.

Non-Trucking Liability Insurance for Joyrides in a Winter Fantasy: Even when your truck is just exploring the snowy landscape of Grant County, this semi truck insurance ensures it’s as protected as a hibernating bear.

Occupational Accident Insurance for Those Braving the Cold (No Squirrels Included): Ideal for your human team members who are out there braving the icy roads, ensuring they’re covered faster than you can say “hot chocolate break!”.

Additional:

Incorporating a bit of snowy humor makes the topic of insurance a bit more fun, especially with the Wenatchee Insurance Agency potentially familiar with the unique challenges of insuring trucks in snow and ice. Just remember, while the snow and ice jokes are light-hearted, ensuring you have the right coverage for all seasons is seriously important. Stay safe and maybe keep your chains and a snow shovel handy, just in case!

Suzie & Matt help run the Enrollment Center in Wenatchee and they get a lot of questions. How to make a payment is a big one. This year we are seeing a bunch of new folks as Cascade Care has introduced Immigrants to the Healthplanfinder.

During the open enrollment period the Healthplanfinder allows for an initial payment once your plan has been selected. The open enrollment period runs from November 1st through December 15th.

Since Washington State has it’s exchange the Washington Healthplanfinder they can add additional enrollment periods. For this year, we are going to January 15th for plans starting February 1st.

Some companies will not ship your insurance policy information before they have received payment so it is an important step.

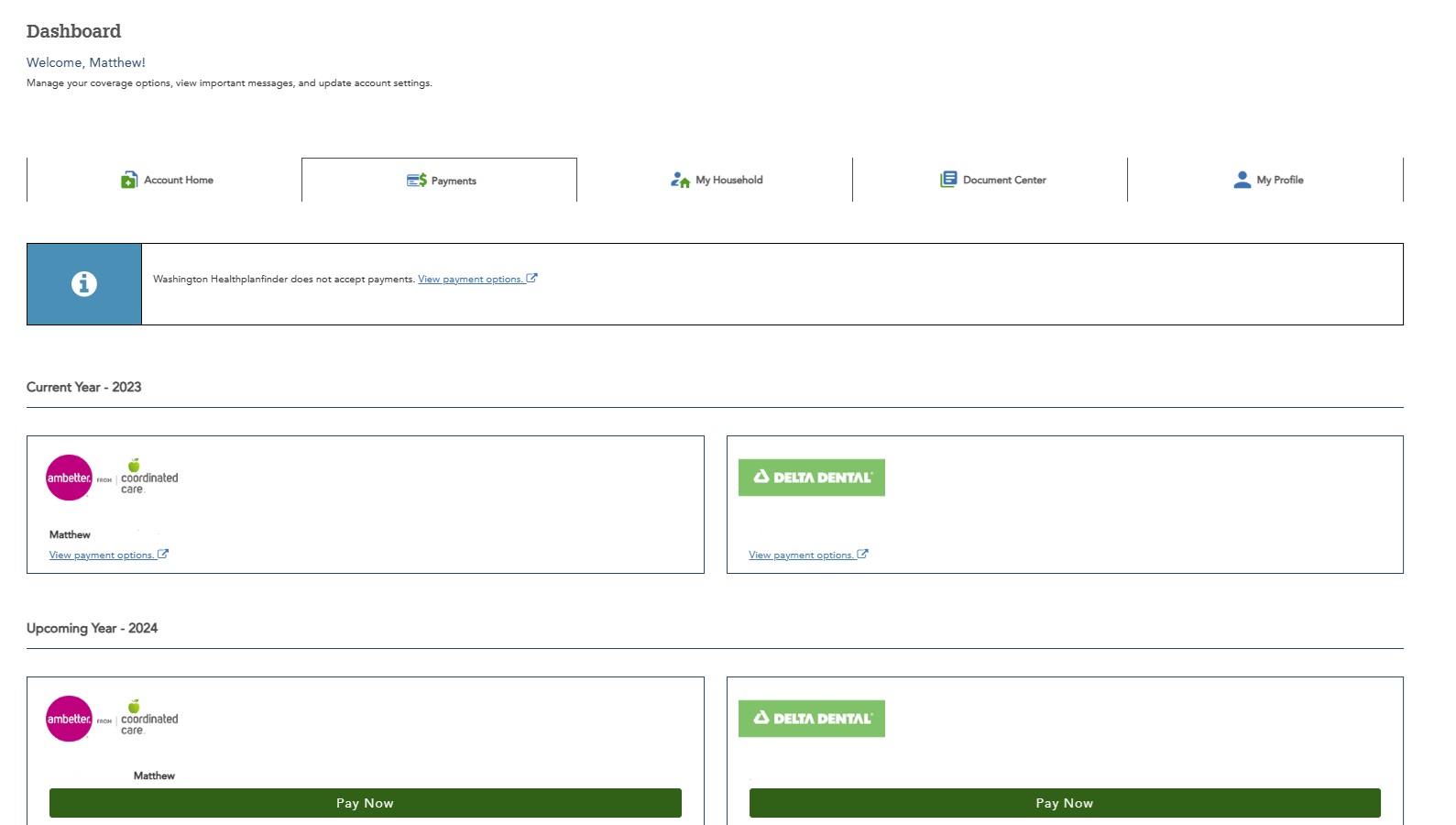

Your main screen will look like this:

Go to the Payment tab, push the Green button, and process the payment. Some companies will allow you to set up the automatic monthly payment here.

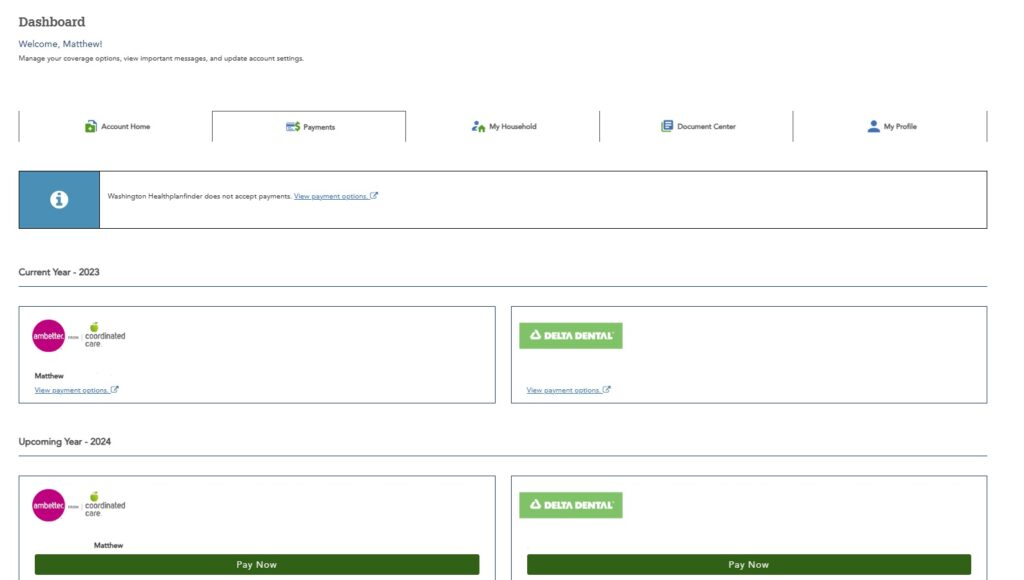

Here is the payment tab.

After the enrollment period

You will want to work directly with the insurance companies. Some will allow for automated payments and some insurance companies work well with brokers to allow for payment processing. (Talk to your insurance broker if this is an option).

The current list of insurance companies and their payment links:

If you enrolled using the Washington Healthplanfinder then you can make an immediate payment using the Washington Healthplanfinder during the enrollment period. If you want to use the insurance company’s webpage then it may take a couple of days for the files to transfer. Making a call to the insurance company can speed up the process.

Age Is Just a Number, Especially When Forgetting Yours: Find an agent who doesn’t just offer senior policies, but also reminds you of your age – preferably someone who celebrates your “29th” birthday with you, annually. We love you checking in, reviewing policies and shopping.

Experience in Senior Discounts, Including Early Bird Specials: An agent who knows the ins and outs of senior discounts is a gem. Bonus points if they can also guide you to the best early bird specials in town. (We like Shakti’s).

A Walking, Talking Medical Dictionary: You want an agent who understands senior health plans better than they understand their grandchildren’s slang. If they can explain your policy options without needing a nap afterward, you’ve struck gold. (As a former pharmacy technician, Suzie can spell Ozempic in her sleep).

Technologically Savvy, But Not Too Savvy: Look for someone who’s tech-savvy enough to email you your policy but still prints out directions from Google Maps. By using an appointment app, it gives us more time to chat.

The Patience of a Saint: This agent doesn’t just have patience; they have the kind of zen-like calm that could rival a tortoise in meditation. They’ll explain the fine print so many times, even your forgetful cousin could recite it.

Remember, finding the right insurance agent should be as satisfying as finding that last piece of candy at the bottom of your purse – a delightful surprise that makes your day just a bit sweeter!

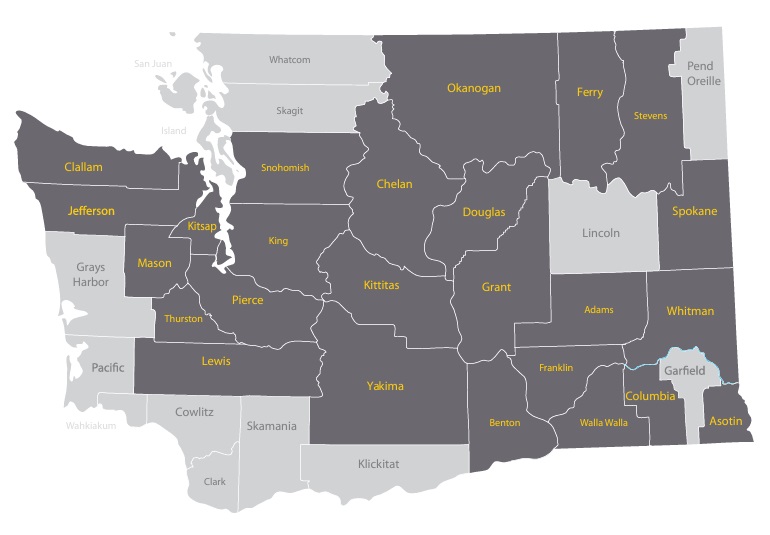

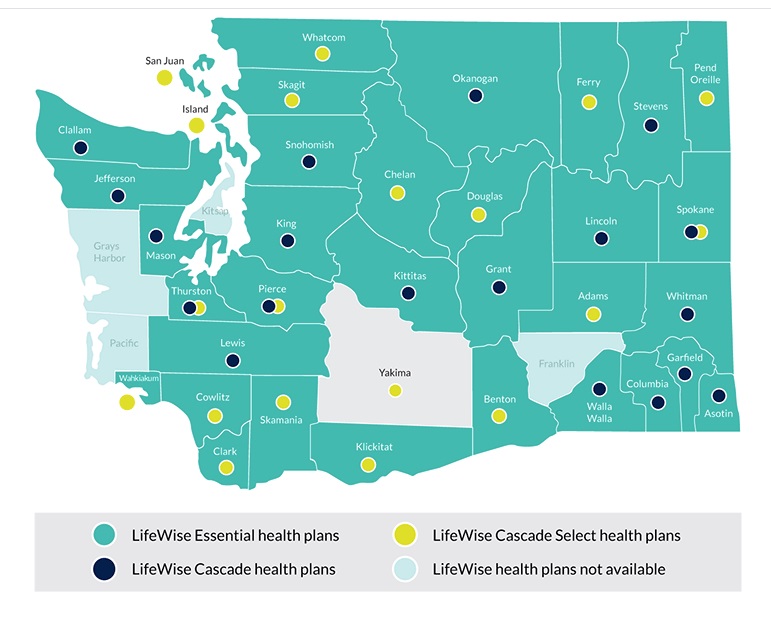

At the Enrollment Center, we get asked a lot about networks from people wanting to understand their plans. There are a lot of assumptions about networks and this is intended to dispel some of those assumptions.

Domestic medical tourism refers to the practice where individuals travel within their own country to access medical treatments or healthcare services that are not available or are of a different quality or more affordable in another region or city within the United States. This can include a wide range of medical services, from major surgeries and specialized treatments to elective procedures and wellness services.

Key aspects of domestic medical tourism include:

Accessibility of Specialized Care: Patients might travel to another part of the country to access specialized medical expertise and advanced treatment options that are not available in their local area.

Avoiding Long Wait Times: In countries where healthcare systems face high demand, patients may face long wait times for certain procedures. Traveling to another region where the wait times are shorter can be an appealing option.

Combining Treatment with Leisure: Some patients might combine their medical treatment with leisure activities, turning their medical trip into a more pleasant experience. This is particularly common in areas known for their natural beauty, cultural significance, or relaxation facilities.

Quality of Care: Patients may perceive healthcare providers in certain cities or regions as being of higher quality than those available locally, prompting them to travel domestically for treatment.

Domestic medical tourism is influenced by factors such as the availability of healthcare services, the cost of care, the quality of facilities, and the reputation of medical practitioners in different regions of a country.

Domestic medical tourism has forced insurance companies to limit their networks to reduce provider costs. There has been a shift from the individual marketplace from Preferred Provider Organization (PPO) plans to Health Maintenance Organization (HMO) to Exclusive Provider Organization (EPO).

In Wenatchee, the most popular clinic is Columbia Valley Community Health Service (CVCH) however there are over 21 Community Health Centers operating 200 Primary Clinics and over 70 Hospitals operating in the Community Health Plan of Washington‘s network.

Lifewise has a variety of different levels, especially pay attention to the Cascade and Cascade Select plans as not every doctor is contracted with every Lifewise Network.

One of the Big advantages to Lifewise is the exclusive access to the Kinwell Clinics located throughout Washington State.

While domestic medical tourism has played a role in reshaping the Washington State Insurance and provider networks, we do have the ability with the three plans to travel to different parts of the state and still be with in network.

Please double check coverage prior to selecting a plan and prior to medical procedures as networks can shift with contracts.

Employers don’t have to offer health insurance. Some employers don’t. I have used the exchanges since I am self employed and there was a gap in coverage for my Veteran’s coverage.

For the United States, the main exchange is Healthcare.gov. If you have enough knowledge, then you can do it yourself or it can help you find someone to assist you.

I work in Washington state. Our state’s exchange is the Healthplanfinder.com. State Run exchanges can have extra benefits for example we get a bonus month for enrollments. My wife and I have been running one of the ten enrollment centers for the state which are located in Wenatchee. We have special rules in that we explain all of the plans on the exchange and are available year-round to assist and answer questions.

Who can help?

Check-in with your state resources and whenever possible use local resources. Health insurance plans are very regional like contracting down to the county level. There is a lot of disinformation out there as you work with more trained professionals the opportunity for understanding increases.

Just in case they need Medicare the Annual Enrollment Period is October 15th through December 7th. Yes, the overlap means that the people assisting people are incredibly busy.

Two groups that can be of further assistance:

Medicare the State Health Insurance Assistance Program. These are volunteers they can explain however they cannot recommend or fill in any insurance gaps.

Once you find a volunteer or broker that you connect with then do not hesitate to set an annual appointment early. Every year review your options and it will reduce surprises in the long run.

Outside of Open Enrollments, there are Special Enrollments

If you qualify for Medicaid or American Indian & Alaska Natives then you can enroll year-round. If you lose coverage or gain immigration status then you can use a special enrollment. Sometimes the state will declare a special enrollment for a disaster. Our office runs every application because special enrollments occur regularly and we want our clients to have the opportunity. If they miss it then they are set for the fall enrollment.

This year we had a large number of people setting appointments in September for their Fall appointments and they were able to spend minimal time waiting for an appointment or chasing a calendar space.

Flood damage is one of the costliest types of home damage every year in the United States. That’s why it’s so important for homeowners in Wenatchee, WA to purchase flood insurance. At Wenatchee Insurance Agency, we offer flood insurance policies that can protect homeowners financially.

The following are four mistakes that homeowners need to avoid regarding flood insurance.

Procrastinating before buying flood insurance

It’s never a good idea to wait before buying flood insurance. You never know when a flood could cause extensive damage to your home. Buy flood insurance now to ensure that you’re covered when disaster strikes.

Neglecting to follow news about increasing flood risk in one’s area

You can’t assume that your area will never be at high risk of flood damage just because it wasn’t when you initially bought your home.

Flood zone maps can change due to community development projects and changes in regional weather patterns. That’s why it’s always important to follow local news on flood zone classifications.

Overlooking details regarding basement coverage

Homeowners with basements need to pay attention to the fine print on their flood insurance policies. Some flood insurance policies limit coverage for basement areas of a home.

You cannot assume that a standard flood insurance policy will cover any basement damage that your home could experience. Basement coverage is an especially important policy detail for homeowners with finished basements.

Relying on home insurance for flood damage coverage

One of the most important things homeowners should know about flood damage is that standard home insurance doesn’t cover floods. You need to invest in a separate flood insurance policy or add a flood coverage endorsement to your home insurance policy to get flood damage covered.

When your home in Wenatchee, WA experiences flood damage, it’s essential for you to have a flood insurance provider you can rely on. Call us at Wenatchee Insurance Agency to get a quote on a flood insurance policy that will give you peace of mind and protect your home’s value.

We like to do cost estimators on property prior to quote. It reduces the chance of a property being underinsured. This is especially problematic when rewriting older policies that have not been maintained and periods of high inflation.

Here we break down the example where your house is valued at $500,000, insured for $400,000, and incurs partial damage worth $50,000 in a fire:

Policy Limit: Your insurance policy covers up to $400,000. This is the maximum amount the insurance company will pay in case of damage.

Damage Assessment: The damage to your home is assessed at $50,000.

Underinsurance Factor: Since your home is underinsured (it’s insured for $400,000 but is worth $500,000), you have only insured 80% of its value ($400,000/$500,000)×100=80($400,000/$500,000)×100=80.

Claim Settlement: Insurance companies often use the “coinsurance clause” in such scenarios. This clause means that if you have not insured your property to at least a certain percentage of its value (often around 80-90%), the insurance company may reduce the payout for partial losses.

Let’s calculate the potential payout:

If your policy has a coinsurance clause requiring at least 80% coverage, you are just at the threshold and your claim might be fully paid.

However, if the requirement is higher than 80%, your claim payment could be reduced. For example, if the requirement is 90%, the calculation would be:

$50,000×($400,000$450,000(90% of $500,000))≈$44,444$50,000×($450,000(90% of $500,000)$400,000)≈$44,444

This means you would receive about $44,444, and you’d have to cover the remaining $5,556 out of pocket.

Out-of-Pocket Expenses: In the scenario where the full claim isn’t covered due to the coinsurance clause, you will need to pay the difference between the claim payment and the actual damage cost.

Policy Review: This example highlights the importance of regularly reviewing your insurance coverage to ensure it matches the current value of your property, especially after significant changes in market value or property improvements. Having a conversation with your local independent agency can save a lot of headaches prior to claims.

The specifics can vary based on the terms of your insurance policy and local regulations, so it’s crucial to understand the details of your insurance coverage and any coinsurance requirements.

If it has been more than two presidents since you have talked with an Insurance Agent then we want to talk with you.

Here are seven types of insurance you should consider:

1. General Liability Insurance: This insurance provides coverage for damage or injuries that might occur due to your job. For instance, if you accidentally damage someone’s property while working, this insurance can pay for repairs. In Washington State, Labor, and Industries will want to have proof on file.

2. Professional Liability Insurance: Also known as Completed Operations Coverage, this coverage protects you against claims where your work is alleged to have caused a financial loss. If a client claims that an error in your work caused them to lose money, professional liability insurance would cover your legal costs and any settlements.

3. Commercial Auto Insurance: If your business involves the use of vehicles, commercial auto insurance is necessary. This provides coverage for accidents, injuries, and property damage related to company-owned or leased vehicles.

4. Builders Risk Insurance: This insurance, also known as Course of Construction Insurance, provides coverage for the project itself from damage or loss due to events like fire, theft, or severe weather conditions. It can be done for new construction or a remodel job.

5. Tools and Equipment Insurance: This insurance covers the cost of repairing or replacing your equipment due to theft or unexpected breakdowns. It does not cover normal wear and tear.

6. Commercial Umbrella Insurance: This insurance provides an extra layer of protection beyond the limits of your other policies. If a claim exceeds the coverage limits of your other insurance, commercial umbrella insurance can cover the excess costs.

7. Surety Bonds: These act as a guarantee that you will fulfill the terms of your contract. If you fail to do so, the bond can pay to have the job completed. Some jobs will require additional bonds if you win the bid.

Remember, the specific insurance requirements can vary depending on the nature of your work and where you operate. Therefore, it’s a good idea to consult with your independent insurance agent to ensure you have the right coverage.

Topics: Contractor Insurance, Business Liability, Surety Bond, Builder’s Risk, Commercial Auto, Completed Operations, General Contractor, Sub, Handyman, LandI Labor and Industries, Tools and Equipment,

Does Medical Crowdfunding work? The American Journal of Public Health found that only 12% of medical GoFundMe campaigns reached their goals and a whopping 16% received no donations at all. Passing a hat to pay for expenses sucks and I would not wish that on anyone.

Let’s keep it light. Here are the top 10 humorous reasons you might consider getting life insurance:

Ghost Support: To make sure your ghost can haunt in style, with the latest ethereal gadgets like the “Boo-Bluetooth” or “Specter-Spectacles.”

Debt Zombie Apocalypse: Life insurance helps ensure that your debts don’t rise from the grave to haunt your family, because the only thing worse than actual zombies is debt zombies.

Funeral Extravaganza: So you can afford a funeral that’s less “sob and sniffle” and more “rock concert with pyrotechnics,” because you always wanted to go out with a bang!

Mortgage-B-Gone Magic: Wave that wand and say goodbye to the mortgage! It’s the financial equivalent of a vanishing act for the ultimate peace of mind.

Kid’s College Fund… or Bail Money: Whether it’s for their education or in case they take after your wild younger days, you’ve got it covered!

Inheritance Roulette: Leave a game of financial Clue for your relatives. “I bequeath my collection of rare cheese labels to… the one who can stand on one leg the longest.”

Guilt-Free Shopping Spree: Gives your partner the chance to indulge in retail therapy without the guilt, because “Honey, it’s what they would’ve wanted.”

Secret Lair Maintenance Fund: Keeps your secret lair in tip-top condition for future generations of family super-villains or superheroes. Your kid could be Batman. Your legacy of mysterious hideouts lives on!

The “I Told You So” Clause: For all the times you said you’d die before going to your in-laws’ house for dinner… and well, you want to be a person of your word.

Santa Replacement Service: Ensures that Christmas remains a jolly affair with a professional Santa to fill your boots. Elves and reindeer rentals are, however, optional extras.

Remember, while it’s fun to add a touch of humor, life insurance is a serious matter that helps provide financial security for those you care about most! We will assist you along the way.

Topics: Wenatchee Insurance, Life Insurance, Term Life, Whole Life, Family Planning, Final Expense, Health, Medicare, Chelan, Okanogan, Leavenworth, Liability,

For nearly a decade we have assisted with Health & Medicare Solutions. We are proud to be selected by the Washington Healthplanfinder to be one of ten Enrollment Centers located in Washington State.